Mise à jour : 24 juin 2011 (Rédaction initiale : 15 juin 2011 )

Parutions : I. Articles Isolés

I-1.34: From copper to fibre: an optimal regulatory policy

ENGLISH

The role of fibre is very important towards connecting to ultra-fast broadband, one of the key action areas of the Digital Agenda. But, Europe is late in its fibre deployment, especially when compared to other advanced economies such as the United States or Japan. At the same time, however, there is still no standard for a European fibre strategy: public as well as private stakeholders are having very different approaches in local FTTx deployment sometimes leading to a waste in private and public funds and being mainly focused on dense areas. This article aims to propose an efficient model for fibre network deployment that can be applied to all European Member States. The model provides high-margin incentives for operators to install fibre network across the whole country, while maximising households’ fibre connection rate through an automatic migration scheme. In a period of weak growth and budget restrictions, the catch-up in ultra-fast broadband internet requires more than ever an efficient policy to maximise the deployment of FTTH at the lowest cost possible to the public. The proposed model serves as an ideal choice given this context.

Alternative operator - Budget - Connexion - Copper network - Cost - Digital agenda - Duplication - Effeciency - Essential facility - Europe - Fiber optic - France - Incentive - Incumbent operator - Infrastructure - Internet - Natural economic monopoly - Network - Price - Provider - Regulatory policy *

* In The Journal of Regulation, these keywords are done by the Editor and not by the Author.

PORTUGUESE

Artigo: Do cobre à fibra: uma política de regulação ótima.

O papel da fibra é muito importante em conexões de banda larga de alta velocidade, uma das principais ações na área da Agenda Digital. No entanto, a Europa está atrasada no desenvolvimento da fibra, especialmente quando comparada com outras economias avançadas como Estados Unidos ou Japão. Ao mesmo tempo, porém, ainda não há um patamar para uma estratégia europeia para a fibra: detentores de haveres públicos e privados têm tido diferentes posturas no desenvolvimento de FTTx local, o que leva às vezes a um desperdício de fundos públicos e privados e sendo sobretudo registrado em áreas de densidade. Este artigo objetiva propor um modelo eficiente para o desenvolvimento da rede de fibra que possa ser aplicado para todos os Estados Membros Europeus. O modelo prevê incentivos altos para operadores para instalar redes de fibra por todo o país, enquanto maximiza a taxa de conexões domésticas de fibra através de um esquema de migração automática. Em um período de crescimento desacelerado e restrições orçamentárias, um novo impulso em banda larga de alta velocidade requer mais do que nunca uma política eficiente para maximizar o desenvolvimento de FTTH ao menor custo possível para o público. O modelo proposto serve como uma escolha ideal dado este contexto.

Operador alternativo – Orçamento – Conexão – Rede de cobre – Custo – Agenda digital – Duplicação – Eficiência – Facilidades essenciais – Europa – Fibra ótica – França – Incentivo – Operador – Infra-estrutura – Internet – Monopólio natural econômico – Rede – Preço – Provedor – Política de regulação*.

* No Journal of Regulation, as palavras-chave são fornecidas pelo Diretor, e não pelo Autor.

ITALIAN

Articolo: Dal rame alla fibra: un’ottima politica di regolazione

Il ruolo della fibra è molto importante per la connessione ad alta velocità, una delle azioni centrali dell’agenda digitale. Tuttavia l’Europa è in netto ritardo per quando riguarda lo sviluppo della fibra, in particolare rispetto all’economia di altri paesi come gli Stati Uniti o il Giappone. Questo si capisce, però, in quanto non esiste uno standard per la strategia dell’Europa in materia di fibra: gli attori privati e pubblici del settore della fibra stanno avendo degli approcci differenti nei confronti della realizzazione dei FTTx, e tali approcci spesso si concludono in uno spreco di investimenti e si concentrano spesso su aree ad alta densità. Questo articolo si propone di trovare un modello efficace per la realizzazione di una rete a fibra in tutti gli Stati membri. Questo modello prevede degli incentivi elevati per gli operatori che installano delle reti a fibra ottica nei loro paesi, e massimizza la percentuale di connessioni a fibra ottica per nucleo familiare con un sistema di migrazione automatico. In un periodo di crescita ridotta e restrizioni di budget, lo sviluppo di connessioni a fibra ottica richiede una politica quanto mai efficace per massimizzare lo sviluppo del FTTH ai minimi costi possibili per i conti pubblici. Il modello proposto costituisce una scelta essenziale, in considerazione del contesto esistente.

Agenda digitale - Budget - Connessione - Connessioni su rame - Costi - Duplicazione - Efficienza - Europa - Fibra ottica - Fornitore - Francia - Incentivi - Infrastruttura - Infrastruttura essenziale - Internet - Monopolio economico naturale - Operatore alternativo - Operatore storico - Prezzo - Politica di regolazione - Rete *

* In The Journal of Regulation, le parole chiave sono responsabilità dell’Editore e non dall’Autore.

SPANISH

Artículos: Del cobre a la fibra : una política regulatoria óptima

El rol de la fibra óptica es de gran importancia en lo que concierne la conexión al ancho de banda ultrarrápida, una de las áreas claves de acción en la Agenda Digital. Sin embargo, Europa se encuentra atrasada en cuanto a su desarrollo, especialmente en comparación con otras economías avanzadas, como la de los EEUU o Japón. No obstante, todavía no existe un estándar para una estrategia europea para la red de fibra óptica; accionistas, tanto privados como públicos, han estado adoptando diferentes acercamientos a la implementación de los FTTx, lo cual suele llevar a un enfoque sobre áreas demasiado densas y al desperdicio de fondos privados y públicos. Este artículo tiene como objetivo proponer un modelo eficiente para el desarrollo de la red de fibras ópticas que podría aplicarse a todos los miembros de la Unión Europea. El modelo provee incentivos de gran margen de ganancias para operadores para la instalación de estas redes de fibras a través del país entero y al mismo tiempo maximiza la conexión rápida de fibras en todas las viviendas facilitado por el uso de un esquema de migración automática. En un periodo de crecimiento débil y restricciones presupuestarias, el “catch-up” en el Internet de banda ancha ultrarrápida requiere ahora más que nunca una política eficaz para maximizar el desarrollo del FFTH y minimizar el coste incurrido por el público.

Other translations forthcoming.

Pièces jointes

The role of fibre is very important towards connecting to ultra-fast broadband, one of the key action areas of the Digital Agenda. But, Europe is late in its fibre deployment, especially when compared to other advanced economies such as the United States or Japan. At the same time, however, there is still no standard for a European fibre strategy: public as well as private stakeholders are having very different approaches in local FTTx deployment sometimes leading to a waste in private and public funds and being mainly focused on dense areas. This article aims to propose an efficient model for fibre network deployment that can be applied to all European Member States. The model provides high-margin incentives for operators to install fibre network across the whole country, while maximising households’ fibre connection rate through an automatic migration scheme. In a period of weak growth and budget restrictions, the catch-up in ultra-fast broadband internet requires more than ever an efficient policy to maximise the deployment of FTTH at the lowest cost possible to the public. The proposed model serves as an ideal choice given this context.

In February 2009, Commissioner Neelie Kroes, Vice-President of the European Commission responsible for the Digital Agenda, talking about the fibre deployment situation in Europe, admitted that “The current rate of new connections – now down to 25,000 a day – is simply not enough to meet our 2020 targets”[#_ftnref1

The historical model for the copper network

What is the starting point? In Europe in general, a copper network deployed by the incumbent operator makes telephone service available across the whole country. This network has supported the development of the low-speed and then high-speed internet. Internet service providers (ISPs) pay an access price to the copper network that is mostly regulated and fixed by National Regulatory Authority (NRA). The price is currently at €8.55/line/month in Europe[#_ftnref3

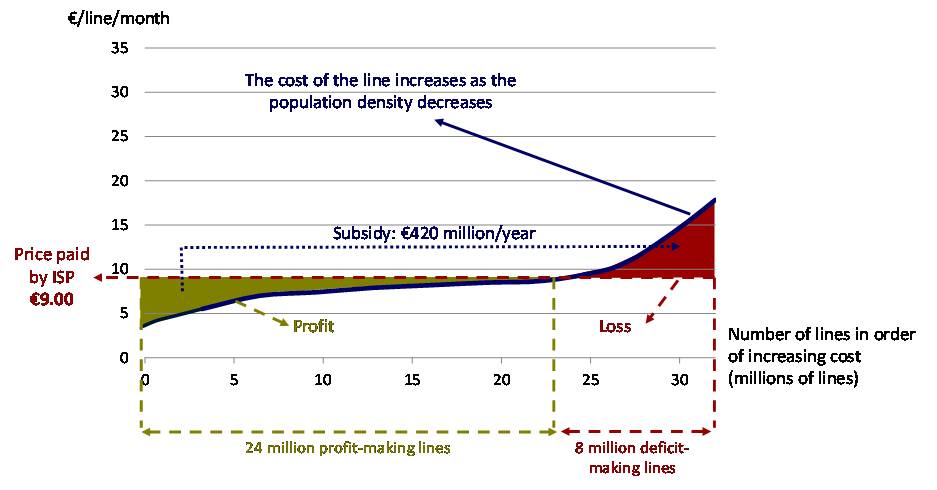

In France, for example, where the access price to the copper network of France Telecom is at €9.00/line/month, a geographical averaging of costs by which 24 million lines finance 8 million lines is in place. These 24 million lines, whose cost is less than €9.00/line/month, incur a profit of €420 million/year and thus subsidise the 8 million lines whose cost is higher than its price[#_ftnref4

Figure 1: Geographical averaging of costs between lines in the copper network in France

{kind=link}

Source: Tera Consultants.

This system allows French ISPs to buy an access to the copper network that let them sell ultra-fast broadband internet at around €32/line/month including tax[#_ftnref6

A transition from copper to FTTH: the efficient regulatory model

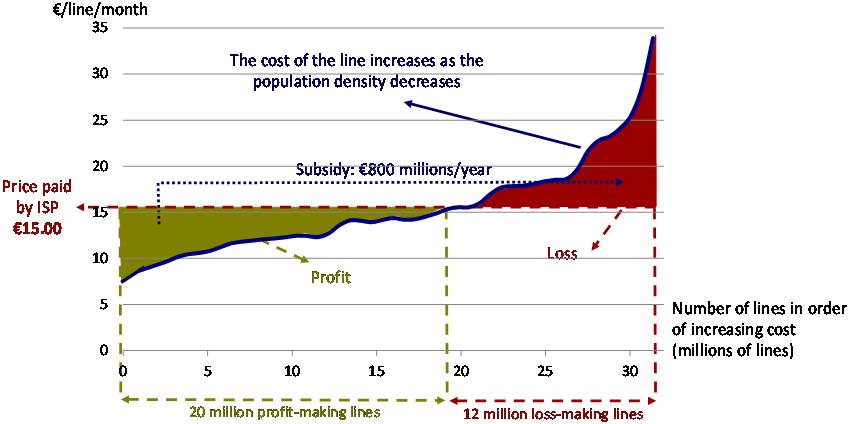

Let us consider the total replacement of the copper network by the FTTH network. This new network is based, like the copper network, on a point-to-point architecture which facilitates fibre unbundling. This network also links the optical distribution frame (ODF) with a minimum capacity of 2000 lines, which is an essential element that allows for a full-fledged competition among all the ISPs across the whole country, including the lines that currently do not enjoy the best of broadband internet. The same profit as the copper network (same WACC) could be applied. The access price to the fibre network paid by ISPs would be the national average cost of all the lines. In this system, with the same geographic averaging as for the copper network, there will be profit-making lines, whose cost is lower than the average price, and loss-making lines, whose cost is higher than the average price. A fund with contributions from profit-making areas should assure the subsidy of loss-making areas. The operating principles of such a fund have already been tested as in the universal telecommunications service.

The FTTH connection rate under this system is automatically 100% since the switch off of the copper network is planned through a mandatory migration similar to that currently in place for the Digital Terrestrial Television for example, or to the successful change from 110 to 220 volts in electrical networks. This further guarantees the profitability of FTTH by maximising economies of scale. The system can also allow residential subscribers who opt for the telephone service only on their fibre access to keep their current price plan, which is €15/line/month VAT included for the European average[#_ftnref7

In order to ensure that the FTTH is deployed in the most efficient manner, a competition for the market could be introduced to choose the most efficient FTTH network operator at the local level.

When this model is applied in France, total investment needed including connection to each accommodation is estimated at €36 billion that is supposed to pay off within 35 years with the same level of profitability as the copper network at 10.4%[#_ftnref8

For ISPs’ consumers, the retail fibre monthly rental charge would then stand between €38 and €39/line/month, equivalent to a 20% price increase compared to the standard broadband over copper monthly rental charge. In return, these consumers would enjoy symmetric internet access at a higher speed of up to 50 times and the possibility to choose any ISP and to have access to any internet service regardless of where they live.

Figure 2: The cost, average price and subsidy for an efficient national FTTH deployment

{kind=link}

Source: Tera Consultants.

The errors of the model chosen nowadays

The efficient model above can be applied to any other country, in Europe as well as elsewhere. However, this has not been chosen as a European standard. In fact, there is currently no European standard at all. A host of different initiatives has sprung up: in Switzerland, the incumbent Swisscom and the utility operator EWZ work together to construct the fibre network in largest cities, in Italy, alternative operators have teamed up for the deployment, in Sweden, the Netherlands or Germany, the municipalities and the incumbents have led the way, in France, on the other hand, both the incumbent and alternative operators have built their own infrastructure, thus leading to a duplication of fibre networks, etc. As a result of these “unorganised” and diverse initiatives, market players and NRAs must now think about how to encourage investment in fibre deployment and migration from copper to fibre. For example, the European Commission issued an NGA Recommendation in 2010 that requires regulator to take into account an investment risk premium to allow for an increase in wholesale access price to the new fibre network[#_ftnref9

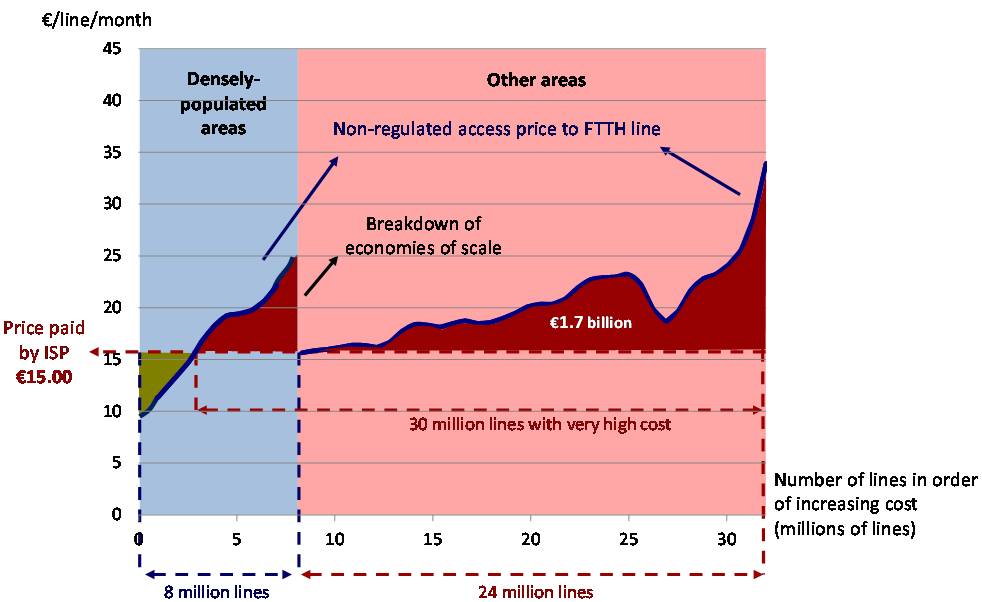

An example of inefficient model is the case in France, where the duplication of FTTH networks takes place in areas classified as "very dense" (148 municipalities and 5.5 million households according to ARCEP). This duplication disrupts economies of scale and leads to an average price of access to FTTH twice as high in very dense areas: it will amount to around €20/line/month vs. €10/line/month if the network had not been replicated. Outside very dense areas, economic rationality reasserts itself: only one operator can reasonably be expected to deploy the FTTH network, France Telcom[#_ftnref11

Figure 3: Cost, disruption and "digital divide" in the current system, the example of France

{kind=link}

Source: TERA Consultants.

In addition, several incumbents in Europe deploy nowadays a FTTH network with the Passive Optical Network (PON) architecture such as France Telecom, Telenor of Norway, Telecom Italia, and A1 Telekom of Austria. This is a technical choice that makes it expensive and difficult to open their network to competing ISPs in the future. In Europe, since no constraint is imposed on the minimum size of the ODF, the incumbent will be free to completely close the market by creating small ODF that the alternative operators will not be able to serve due to low economies of scale. Service-based competition will be all the more weakened since ex ante regulation of offers enabling access to FTTH networks is still at a hypothetical stage in many European countries. Instead, it should be decided a priori and not a late remedy to address certain malfunctions.

Obviously, in the current models in Europe, there is no longer any guarantee of a deployment of FTTH to all households, especially since the deployment cost in non-urban areas could be very high. For instance, in France, outside very dense areas, FTTH access prices vary depending on the municipalities, from €12 to €34/line/month. This risk is increasing the digital divide whereas in fact, people living in rural areas would benefit more from FTTH than city dwellers because internet connection speed on fibre does not decrease with distance, contrary to the copper case. On top of this, even if fibre deployment would perhaps be extended to rural areas, there would be no guarantee of homogenous price in all areas of the country. This is already the case in the Netherlands –one of the most dense and homogeneous country from a geographic point of view in Europe-, where fibre deployment is in an advanced stage compared to other European countries but where access price to fully unbundled ODF varies between €12.14/month and € 17.71/month[#_ftnref13

Conclusion: an absolute necessity to revise the models adopted in Europe

There exist circumstances where competition cannot work. Lawyers call that “essential facility”, economists “natural monopoly”. In these circumstances, regulation is needed. The situation of the local loop of wired telecommunications networks falls within this issue: the duplication of infrastructure increases the costs to such an extent that no gain in competitive efficiency is able to offset the cost of this duplication. The replacement of copper by fibre does not change the technical and economic fundamentals of wired local loop. Why? This is due to the fact that most of the fixed costs of this local loop consist of civil work, construction, engineering and labour, items not subjected to the digital technology progress.

It is therefore indispensable to have a comprehensive review of current regulatory model in order to overcome the digital divide, to ensure the maximum FTTH deployment in Europe with the lowest cost possible by introducing effective competition everywhere and to promote the dissemination of innovations in the digital economy of the future. The digital divide must be resolved and must not be turned into an economic abyss.

[#_ftn1

[#_ftn2

[#_ftn3

[#_ftn4

[#_ftn5

[#_ftn6

[#_ftn7

[#_ftn8Notice explicative de l’outil de simulation de la tarification du génie civil de boucle locale en conduite de France Télécom - May 2010).

[#_ftn9

[#_ftn10http://www.etno.eu/Default.aspx?tabid=2381]; ECTA’s proposal is based on the WIK’s study available at [http://www.ectaportal.com/en/REPORTS/WIK-Studies/WIK-Study-Apr-2011/->http://www.ectaportal.com/en/REPORTS/WIK-Studies/WIK-Study-Apr-2011/]

[#_ftn11http://www.autoritedelaconcurrence.fr/user/standard.php?id_rub=368&id_article=1417]

[#_ftn12

[#_ftn13th quarter results 2010, page 73, available at [http://www.kpn.com/corporate/aboutkpn/investor-relations/presentations/analyst-presentations.htm->http://www.kpn.com/corporate/aboutkpn/investor-relations/presentations/analyst-presentations.htm].

[#_ftn14

votre commentaire