Updated: Nov. 25, 2010 (Initial publication: Oct. 14, 2010)

Releases : I. Isolated Articles

I-1.20 : Regulation by Trust : the example of Stress Tests

ENGLISH

On July 23, 2010 was published the awaited European-wide stress test, a mechanism designed by regulators to restore trust in markets through the mean of transparency. This paper examines the effect of trust on market from an economic perspective as well as from a sociological one. The paper demonstrated how trust, because it aims at achieving transparency which is Regulation’s number one tool, is not only necessary to economic growth but also participates to fulfilling regulatory objectives, such as market stability, risk prevention and consumer protection. Indeed, because Regulation is a mechanism aiming at preventing market failures, it needs as many tools, such as sociological ones (e.g. incentives) it may use to achieve such aim. The paper suggests that transparency is a tool for Regulation since it acts as a communicating vessel between regulatory objectives (microprudential) and supervisory ones (macroprudential), which both contribute to Regulation’s broader objective: the stability of a system.

FRENCH

Article: la régulation par la confiance: l'exemple des stress tests

Le 23 juillet 2010 a été publié le très attendu stress test à l'échelle européenne, un mécanisme conçu par les régulateurs pour restaurer la confiance dans les marchés par la transparence. Cet article examine les effets de la confiance sur les marchés dans une perspective économique et sociologique. L'article démontre en quoi la confiance, parce qu'elle a pour but d'installer la transparence, premier objectif de la Régulation, n'est pas seulement nécessaire à la croissance économique, mais participe également à l'accomplissement d'objectifs régulatoires, comme la stabilité du marché, la prévention du risque et la protection du consommateur. En effet, parce que la Régulation est un mécanisme visant à empêcher les défaillances de marché, elle a besoin d'autant d'instruments, y compris sociologiques (p.ex. les incitations), dont elle peut avoir usage pour atteindre cet objectif. L'article suggère que la transparence est un outil pour la Regulation puisqu'elle joue le rôle de transmetteur entre des objectifs régulatoires (micro-prudentiels) et des objectifs de supervision (macro-prudentiels), qui tous deux contriibuent à l'objectif plus large de la Régulation: la stabilité d'un système.

GERMAN

Artikel: Durch Vertrauern regulieren: das Beispiel den Stress Tests

Am 23. Juli 2010 wurden die erwarteten Ergebnisse den europaweiten Stress Tests bekanntgegeben. Diese Tests wurden von den Regulierungsbehörden dazu erfasst, um das Vertrauern auf Märkten durch Transparenz wiederherzustellen. Dieser Artikel erforscht die Auswirkung von Vertrauern auf Märkten auf einer ökonomischen und soziologischen Perspektive. Er zeigt, inwieweit Vertrauern, das den ersten Ziel der Regulierung, die Transparenz, einsetzen soll, nicht nur notwendig für die Wachstum ist, sondern auch für die Durchsetzung von Regulierungsziele, wie Marktstabilität, Riskverhütung, und Verbraucherschutz. Zwar ist Regulierung ein Mechanismus, das darauf zielt, Marktversagen zu vermeiden, sie braucht so viele Instrumente, einschliesslich soziologische Instrumente (z.B. Anreize), die sie brauchen könnte. Der Artikel deutet an, dass Transparenz ein Instrument der Regulierunh ist, da sie die Übertragung von Regulierungsziele (mikroprudentiel) und Überwachungsziele (makroprudentiel) erlaubt, was zum breiten Ziel der Regulierung beiträgt, und zwar die Systemstabiliserung.

SPANISH

La regulación a base de confianza: el ejemplo del estudio del estrés

El 23 de julio del 2010 fue publicado el muy esperado estudio del estrés, que se llevó a cabo a través de toda Europa, lo cual es un mecanismo diseñado por reguladores para restaurar la confianza en los mercados utilizando el valor medio de la transparencia. Este informe examina el efecto de la confianza sobre el marcado desde una perspectiva económica al igual que desde una perspectiva sociológica. El informe demuestra que la confianza, precisamente porque su objetivo es la transparencia que es el instrumento primordial de la Regulación, no sólo es necesaria para el crecimiento económico, sino que también contribuye a la realización de los objetivos regulatorios, como la estabilidad del mercado, la prevención del riesgo y la protección al consumidor. Por lo tanto, ya que la Regulación es un mecanismo cuyo objetivo es prevenir los fallos del mercado, necesita de la mayor cantidad de instrumentos posibles, como instrumentos sociológicos (por ejemplo, los incentivos), para cumplir con su meta. El informe sugiere que la transparencia es un instrumento para la Regulación ya que actúa como una nave comunicativa entre los objetivos regulatorios (microprudencial) y los objetivos de supervisión (macroprudencial), que juntos contribuyen al objetivo más amplio de la Regulación: la estabilidad del sistema.

ITALIAN

Articolo: Regolazione attraverso la fiducia: l’esempio degli stress test

Il 23 luglio 2010 é stato pubblicato il tanto atteso stress test a livello europeo, un meccanismo ideato dai regolatori al fine di rassicurare i mercati attraverso la trasparenza. Tale studio esamina gli effetti della fiducia sul mercato da un punto di vista economico e sociologico. Lo studio dimostra come la fiducia, puntando a raggiungere una maggiore trasparenza, meccanismo primario della regolazione finanziaria, non é solamente necessaria per la crescita economica ma contribuisce inoltre a raggiungere gli obiettivi dei regolatori come la stabilità del mercato, la prevenzione del rischio e la protezione dei consumatori. Inoltre, poiché la regolazione é un meccanismo che vuole evitare i mancati funzionamenti del mercato, sono necessari per raggiungere tale scopo diversi strumenti, tra cui quelli sociologici (ad esempio gli incentivi). Questo studio suggerisce che la trasparenza é uno strumento di regolazione dal momento in cui costituisce il vaso comunicante tra gli obiettivi della regolazione (micropudenziale) e quelli della supervisione (macroprudenziale). Entrambi questi obiettivi contribuiscono al più ampio obiettivo della regolazione: la stabilità di un sistema.

On July 23, 2010 was published the awaited European-wide stress test, a mechanism designed by regulators to restore trust in markets through the mean of transparency. This paper examines the effect of trust on market from an economic perspective as well as from a sociological one. The paper demonstrated how trust, because it aims at achieving transparency which is Regulation’s number one tool, is not only necessary to economic growth but also participates to fulfilling regulatory objectives, such as market stability, risk prevention and consumer protection. Indeed, because Regulation is a mechanism aiming at preventing market failures, it needs as many tools, such as sociological ones (e.g. incentives) it may use to achieve such aim. The paper suggests that transparency is a tool for Regulation since it acts as a communicating vessel between regulatory objectives (microprudential) and supervisory ones (macroprudential), which both contribute to Regulation’s broader objective: the stability of a system.

On July 23, 2010 was published the awaited European-wide stress test, a mechanism designed by regulators to restore trust in markets through the mean of transparency. More than a year after the US (May 2009) but less than a year after a first but criticized attempt in Europe (the first tests did not encompass as many banks and were not published), the EU finally responded to the International Monetary Fund’s calling (IMF) for a coordinated and transparent series of tests on European banks. In the words of the Committee of European Banking Regulators, stress tests are a “risk management tool that has been used for a number of years now, both by banks as part of their internal risk management practices and by supervisors to assess the resilience of banks and of financial systems in general to possible shocks. Stress tests assess adverse and unexpected outcomes related to a variety of risks, and provide an indication of how much capital might be needed to absorb losses would the shocks that have been assumed actually occur”[1].

These tests are prepared in order for banks to subsequently either disclose their resistance to drastic economic conjecture, or to take notice of their failure to do so and consequently recapitalize. After a first series of tests in Europe which were deemed by investors as inconclusive, and after a second crisis in 2010 regarding sovereign debts which highly participated to a new wave of doubt on the solidity and the inter-connection of the banking and financial sectors, the Euro area could no longer ignore the IMF’s recommendation and stay so far behind the US in terms of market transparency and risk disclosure[2]. Economically speaking, these tests have a triple purpose: first, forcing the weakest banks to recapitalize, which should downgrade their aversion to lend and therefore finance new projects (so called debt-overhang, i.e. such aversion which hinders the growth of the economy) ; second, at a time when States intend to render their solvency credible, it is useful for them to reduce the risk that they be once again called on as lender of last resort; last but not least, these tests have a strong regulatory purpose: they were mainly carried out in order to counter any rumors on the “economic health” of banks, which should restore trust on inter-bank[3] market and therefore limit the risk of a new liquidity crisis, i.e. the risk that markets fail due to systemic panic[4]. From this standpoint, trust becomes a regulatory tool.

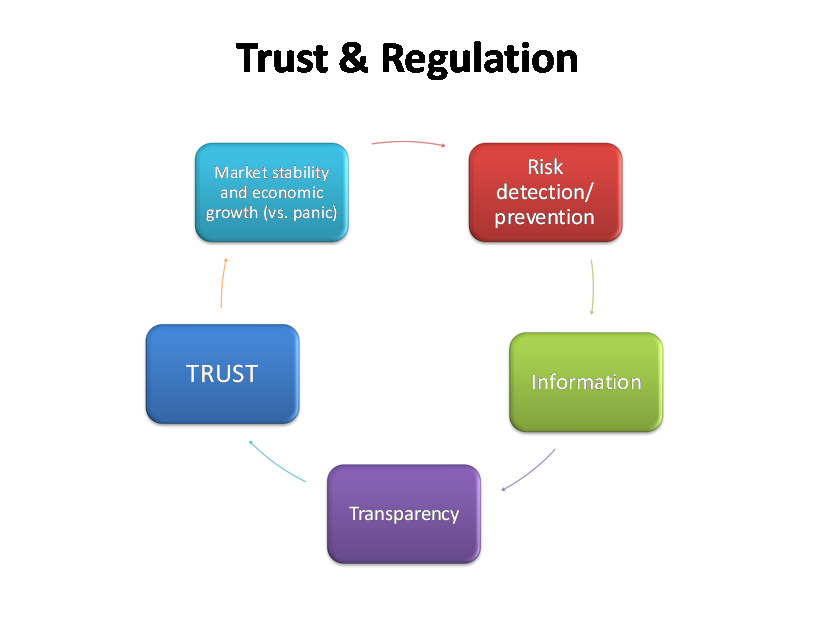

Indeed these tests, the criterions of which undergo today much critics, have however a greater purpose than solely revealing bank’s exposure to sovereign debt or forcing those which did not pass the test to recapitalize: tests aim at trumping the alleged systemic risk remaining from the crisis or any future risk similar to it, and at replacing such rumors by solid information. After two years in the dark, investors can finally make up their own mind on the risk involved in investing on a market and an economy which principally revolves around banks, and therefore around their solidity. From an economist standpoint or even a political one, the idea behind stress tests is to reboot the economy, since only the transparency required by them can restore trust on markets, which is the only way to restore economic growth. In the words of the IMF, “the overarching policy challenge is to restore financial market confidence without choking the recovery. In the euro area, well-coordinated policies to rebuild confidence are particularly important. As discussed in the July 2010 Global Financial Stability Report (GFSR) Update, immediate priorities in the financial sphere include: making the new European Stabilization Mechanism fully operational, resolving uncertainty about bank exposures (including to sovereign debt), ensuring that European banks have adequate capital buffers, and continuing liquidity support”. Such information, should it be made public, have the sole purpose of restoring trust on markets. Therefore, the macro-economic and prudential equation connecting trust to market stability can be summarized as following:

Transparency = Confidence = Economist Growth (transparency only being the consequence of the legal powers given out to regulators, but not of markets functioning which by definition are irrational when self regulated).

But the link between confidence and transparency also serves as a communicating vessel to reach certain regulatory objectives (different from mere economic ones, such as economic growth, but in connection to prudential ones, such as market stability), that is certain equilibrium that markets would not otherwise produce when self regulated: risk detection (produced by transparent information), risk prevention (any loss of confidence in market creates a systemic risk of panic) and consumer protection (information given to investors so they make confident decisions).

Why is trust a tool to regulation?

These tests perfectly serve the purpose of financial regulation. Indeed, financial regulation, which revolves around the goal which was set for it by political decision, which, in the case of finance, is to prevent systemic risk and to protect investors (both through either information, registration, transparency, lack of conflicts of interest etc.), need to use as many tools as possible to fulfill the sought out goal. Economic law, which is at the same time concrete yet teleological, does not consider confidence as a pre-established object (it is not produced by the sole functioning of self regulated markets) but rather as an item which must be built, since it is the key to systemic risk management.

In the case of stress tests, regulation resorts to sociological instruments to achieve its purpose. Indeed, because financial regulation is mainly about risk prevention, which demands as much transparent information (symmetric information rather than asymmetric) as market participants possess, regulation incite markets participants to cooperate in restoring transparency on market and therefore restoring investors confidence, as only the latter will permit markets to efficiently function again. Through the mechanism of incitation, by inducing banks to disclose information because only such data will restore market’s confidence and therefore participate to regenerate their business, regulation can therefore obtain transparency on markets which is the shortest route to risk prevention. Indeed, regulation, when searching to prevent risk on markets, cannot solely rely on the law or the State to command that financial products be simpler and safer and that their originators communicate on them. But what regulators can do, along with exploiting their legal powers, is to incite them to do so. “La théorie des incitation est le mode libéral de régulation des marchés. L’incitation est un mode ex ante d’intervention qui conduit l’agent à adopter un comportement conforme au but recherché, ici la sécurité du service pour que les investisseurs y recourent en confiance, parce qu’ils y ont intérêt. Plus besoin dès lors de force obligatoire exogène, ni de sens moral. L’appât du gain accroît la vertu du système, selon la classique conception d’Adam Smith »[5].

Therefore, from a regulatory point of view, investor’s confidence, because it requires transparency, serves the purpose of regulation. In regulatory thinking, because the goal required is systemic risk prevention, which calls for as much information as possible only available if total transparency is imposed, then transparency will need to be required from markets participants which will only agree to do so because trust is the key to economic growth and to their own survival. Therefore, because teleological regulatory law has a bottom up approach (it starts from the identified goal then looks for the right tool to fulfill it), the equation can be consequently summarized:

Systemic risk prevention and consumer protection = information = transparency = confidence. In regulatory thinking, confidence is only a consequence of the goal to fulfill and the tool to reach it. In a nutshell (see figure 1) risk prevention requires information that will only be given out by market participants (such as banks) because through transparency can be gained confidence (such as confidence in inter-bank market) which is the key to economic growth.

{kind=link}

Moreover, because financial regulation is also about consumer protection, imposing transparency requirements to banks also participates to investors protection, since they too need to be well informed in order to carry on due diligence whilst investing on markets. In both equations, the core is transparency (see figure 2, II) C).

Therefore, we will study why is trust so important on markets that regulators use it as a tool to get transparency on markets and therefore reach risk prevention (I)? The criterion used to run these tests surely play an important role in their efficiency when it comes to restoring trust on markets (II), although it appears as the mere effort to turn markets into more transparent ones suffices to do so, besides the many critics regarding their conduct (III).

I) Why is trust needed on unstable and unsecured markets such as post crisis financial markets?

A) What is trust[6] ?

Trust can be defined as the act of putting one’s self interest in the hand of another person or institution, in the view that some good will come out of it. For example, in business law, the weaker party may enter a relationship which does not play in his favor as long as he may check out of it at all times, should he get the information that the relation has turned against him. “This explains why transparency is at the heart of financial markets, because the weak party can use it at its will: stay the owner of a security or fly off to buy others. Therefore, financial markets communicate trust, because normally, the listing of securities reflects the economic value of the company which issued them, and the market liquidity offers at all time to minorities a right to exit”[7]. But for the game of trust to work, for trust to be rational and a tool for a stable market, individuals need to be assured that the system works in their favor, even when being the weaker party (for example, the unadvised investor), as they will trust that the system will preserve them from financial products or institutions interested into causing them harm. Indeed, “presque toute transaction commerciale, et en tout cas celle dont l’exécution s’étale dans le temps, a en elle-même un élément constitutif de confiance. On peut soutenir que la plupart des situations d’arriération économique dans le monde peuvent être expliquées par un manque de confiance mutuelle »[8]. Therefore, beyond externalities and transactions costs, markets imply a certain amount of communication between individuals, even temporarily, as it allows them to stay in contact or trade objects. Trust is a binder, which renders possible that individuals do not evolve on markets completely atomized. In this view, it is surprising that economists would evacuate any reference to the feeling of trust when building economic reasoning on calculation, as it blinds them from a majorly important human phenomena on markets[9].

That is why financial markets need to inspire such confidence in their system, especially because they are self deating (autoréalisateur). Because the trust that investors put in them is their essence, its loss automatically provokes a major systemic risk (i.e. panic, especially on markets in which systematically important institutions conduct business).

From a legal point of view, the law can produce trust as it is the natural weapon against dangerous products (such as financial services) or persons. This brings up the economic theory of games: who can be trusted[10]? And why should regulation care about confidence on markets?

B) Why need trust?

From an economic standpoint, confidence is crucial for market liquidity. Macroeconomic liquidity (the quantity of monetary assets available in the economy) is different from market liquidity, which refers to the capacity of the market to absorb financial assets quickly and without any significant fall of prices. Whereas the first is permanent and is more exposed to long term economic phenomenon, market liquidity is more fragile. It demands confidence to exists, confidence in the quality of traded assets and in counterparties, and may therefore become suddenly rare should such trust in the system (the system being made up of its content, financial titles, and its containers, counterparties) should come to disappear. Therefore, even though, by definition, investors do take risk on financial markets, they need at least to have faith in the solidity of the system which supports such trades. Therefore, investors may accept a certain amount of moral hazard to enter their trade, as long as they trust the system (e.g. a non complex network).

But, the famous theory of moral hazard, which is at the heart of liberal markets and entails that the sum of particular interests adds up to building the general interest, suffered a lot with the crisis. But in times when the danger of systemic catastrophe arises, the global comes first rather than the perseveration of natural market mechanisms such as moral hazard. The crisis therefore conducted regulators to focus on the detection of any financial markets’ specificity which can, even in good time, constitute a threat or build tensions. This is currently the essence of macro-economic prudential supervision, which proves that regulating financial markets in not merely about regulatory measures (which command markets to uphold certain equilibriums which they could not otherwise create on their sole initiative) but also prudential supervision. If the theory of moral hazard failed to manage behaviors on such self regulated markets, it is because their complexity has become unprecedented. Andrew Haldane[11] (Executive Director, Financial Stability, Bank of England) demonstrated that the financial system is a complex adaptive system, and he applied to the financial sector some of the lessons learned from other network disciplines – such as ecology, epidemiology[12], biology and engineering –, in order to detect the structural vulnerabilities that have built-up over the past decade in the financial system. Complexity can basically take two forms: first it may integrates financial instruments (structured products), because the recent financial innovation increased further network dimensionality, complexity and uncertainty. Second, complexity can appear in the structure of financial systems themselves, as it relies on the interdependence between actors and multiple counterparties. Indeed, contamination of risk requires a network, the architecture and the structure of which constantly evolves due to financial innovation and regulations arbitrage.

This growing complexity had many consequences; the most important to our interest here being that it increased and spread uncertainty[13]. Complex networks have certain characteristic such as non-linear financial dynamics, a dimensionality and hence complexity which amplifies “materially Knightian uncertainties” in the pricing of assets – causing seizures in certain financial markets[14]. « L’incertitude en elle-même a des conséquences considérables. Comme le montrent Caballero et Krishnamurthy, les épisodes de repli vers les valeurs sûres (flight to quality) et la thésaurisation de liquidité (liquidity hoarding) peuvent s’expliquer par un « changement de régime » consistant à passer d’un environnement dans lequel les risques peuvent être mesurés et des probabilités attribuées aux différentes situations à un monde de totale incertitude. Cette analyse permet de rationaliser et de mieux comprendre le gel de la liquidité et du marché observé en août 2007, puis de nouveau en septembre 2008. Face à ces réactions sans précédent, les autorités se sont demandé si « le marché avait connaissance d’informations dont elles ne disposaient pas ». En fait, les intervenants de marché savaient qu’ils ne pouvaient pas savoir. Comme ils étaient directement impliqués, ils étaient conscients de leur incapacité à maîtriser parfaitement la complexité dont ils étaient les auteurs. Ils ont donc agi en conséquence »[15]. Therefore, it appears as the key to confidence, which comes as the opposite of uncertainty, is information, or more exactly the lack of asymmetry of information. By imposing stress tests, regulators force information out of company and markets and therefore offer a remedy to uncertainty[16]. Moreover, although they cannot avoid the complexity of market, they shed some light on its roots (see below, the information given by banks on capital), which permits analysts to draw a map of the system and get a hold of its complexity and the connection between institutions, as well as their viability and solvency.

Therefore, the IMF was the first to require similar stress tests in Europe than to what had been done in the US. In 2010, the IMF still supported such view, and, in its report “Restoring Confidence without Harming Recovery”, the IMF describes that “downside risks have risen sharply amid renewed financial turbulence. In this context, the new forecasts hinge on implementation of policies to rebuild confidence and stability, particularly in the euro area. The euro area projections also hinge on (…) successful implementation of well-coordinated policies to rebuild confidence in the banking system. As a result, financial market conditions in the euro area are assumed to stabilize and improve gradually[17]”.

Economists could not agree more: in order to reassure investors on the solidity of the system and the amount of engagement and interconnection markets participants are involved in, eight economists, French and German, publicly called for European stress tests to restore trust and therefore economic growth: “il est clair qu’un système bancaire souffreteux, pollué par des banques zombies, constitue un obstacle majeure à la reprise économique. Ensuite, le système bancaire n’en finit pas de générer des dysfonctionnements, tant que les pertes ne sont pas complètement reconnues et divulguées. Un système bancaire défaillait serait particulièrement préjudiciaire pour l’Europe, où les économies sont beaucoup plus dépendantes des financements bancaires qu’aux Etats-Unis. Or de sérieuses inquiétudes demeurent quant à l’état du système bancaire européen : les information disponibles ne sont pas satisfaisantes et les marchés financiers, comme l’opinion publique, accordent peu de crédit aux documents comptables publiés par les banques »[18].

One recognizes here the obsession that took hold of the entire financial and banking world in 2008 after the subprime crisis: the hunt to disclose who held and for what amount the so called “toxic assets” (such assets, usually assets backed securities which, due to the real estate bubble, had become illiquid and therefore flawed financial institution’s balance sheets). As Eric Chaney declares on these stress tests, « si l’on avait eu cette transparence sur les produits structures au moment de la crise des dérivés de crédit (des « subprimes » en particulier), cette dernière aurait sans doute été moins longue [19]». In 2010, the new witch hunted by analysts, is exposure to sovereign debt. This is the reason why these tests were finally organized, in order to shed the light on who holds, and for what amount, sovereign debts. Indeed, markets tend to focus on a particular “hot potato”, which indeed may be representing a certain amounts of risk for market stability and liquidity. In order to maintain certain equilibrium on banking and financial markets, for example by shielding them from systemic panic (caused by investors’ the lack of confidence) and therefore systemic risk, regulators must therefore find the right balance between efficient markets (growing economy) and preserving investors from panic and lack of confidence, which demands transparency and information. Therefore, regulation cares about confidence because not only does it insure stable market and economic growth, but also because it participates to bringing markets information and transparency (on company, products, regulators etc.), which is financial regulation’s favorite device.

II) How to obtain trust on markets?

On self regulated markets, conflict is the rule and no alliance is bound to last. This is why the law is market’s natural instrument, because they are of the same nature: built on defiance[20]. But what can the law do faced with the complexity of products and market networks? Because even when a radical simplification of things could mean to resort to the legal force of prohibition, for example by forbidding securitization or a bank to possess in its trading book sovereign debt, Economic law’s adequacy nature requires that it reflects its objects. And, «à la supposer supportable, l’économie demeure libérale et les lacunes juridiques correspondent à des libertés et il faut mieux encadrer qu’interdire. Ainsi lors que le risque du service financier s’est transformé en catastrophe générale, l’arme pour arrêter la crise systémique est l’arme budgétaire, qui est le monopole des organes politiques des Etats[21] et dont le droit ne dispose pas »[22]. Similarly, States cannot either be the exclusive mechanism which can maintain markets stable and equilibrated, the budgetary weapon being an exceptional resort (President Obama recent Wall Street reform actually forbidding it from now on). Therefore, if neither the law nor the State can be the exclusive solution for managing an unstable economy, another mechanisms, such as regulation, which supposes that the three be mixed, is required. In the case of stress tests, it was for regulators, in a coordinated and transparent manner, to take the responsibility to restore trust in markets in order to dissolve any systemic risk. In order for stress tests to be efficient, European regulators (B) had to follow certain guidelines (A).

A) The authentic stress test

First of all, stress tests as they were conceived theoretically consist of evaluating banks’ solvency to come (capital adequacy ratio) under certain collective economic and financial hypothesis. Such technique is not without flaws, since summing up risk distribution in two or three scenarios has to be somewhat arbitrary. But in May 2009, American stress tests on 19 banks permitted to publish these banks’ need in capital and therefore allowed the American financial market to restore a certain amount of stability, which had been lacking for months[23]. These tests were bound to show that a new economic shock would be manageable by financial companies, thanks to the publication of detailed data bank by bank. Rumors stopped, and the incentive to do the same in Europe grew stronger, despite rivalries between Europeans and national regulators.

A first range of tests was completed in 2009 in Europe, but were only carried on 26 banks (against 91 in 2010), at the national level, with few coordination on macroeconomic hypothesis and with only aggregated publication (rather than bank by bank) available at the discretion of national regulators which involved a important costs in terms of informational content of results (such results ran the risk that they be left to the discretion of national regulators and that methods used were hardly the same for all countries). Under such circumstances, the temptation is important for national regulator to pretend regulators’ national banking champions are healthy. Such procedure may not restore confidence on markets, which is highly required by European economies in times of crisis and urgency.

On the contrary, a “trustworthy” test needs particular specificities to have significant impact on investors. First of all, these tests must be based throughout Europe on the same macroeconomic scenario, the same value rules and the same economic shock hypothesis. Banks must be simultaneously submitted to them, as well as the disclosure of their result, which must be made bank by bank. Moreover, supervision of these tests and their data gathering must be centralized[24]. Finally, stress tests require that authorities be ready to make public without delay how they intend to manage insolvent institutions – including in Europe those engaged in important transnational operations. But as eight economists suggested, such an approach does not require that any official transfer of authority from national to European regulators be made[25]. Such is more or less what has been done in 2010 in Europe.

B) Methods, scenarios and requirements

European tests were finally launched under the supervision of the European banking regulator (the Committee of European Banking Supervisors - CEBS), and revealed on July 23rd 2010.

There have been conducted on a sample of 91 European banks (which represents 65% of the total assets of the EU banking sector as a whole) and required the cooperation of national supervisory authorities from 20 EU Member States[26].

CEBS “in close cooperation with the ECB, the European Commission and participating national supervisory authorities”[27], developed the methodology and the common assumptions for the tests. It was left for the ECB to develop the macro-economic and sovereign shock scenarios and parameters. The ECB proposed the size of the haircuts[28] to be used in the assessment of the impact of the sovereign risk on banks holdings of sovereign debt instruments, and probabilities of default and losses given default. CEBS thereafter was in charge of the EU-wide coordination of the exercise. “Amongst others, a network of national stress testing experts has peer reviewed the results and CEBS has performed extensive cross-checks in order to ensure consistency and comparability of the results”[29] (it also added certain parameters to the micro-economic parameters chosen by the Commission and national regulators, such as the evolution of the real estate prices). Finally, each national supervisor was in charge of undertaking the tests with its banks and of confirming their individual results.

Several scenarios, three in total, were designed: one testing banks’ Tier 1 capital ratio under a benchmark scenario for 2010 and 2011, one similar to the first but under “adverse” conditions, and one, within this adverse scenario, faking a sovereign shock (reflecting adverse conditions in financial markets). They all take into account macro-economic parameters (GDP, unemployment, interest rate assumptions or inflation etc.) in Europe, the US and the rest of the world, a degradation of financial markets and a shock on central bank policy rates. However, no scenario foresees a States’ default, and only a small part of banks’ sovereign debt had to undergo the regulators’ scenario (see below, III). The main focus of the test is not on liquidity risk itself but on capital adequacy (i.e. it tests the bank’s capital adequacy ratios’ capacity to stay above 6% under the three scenarios)[30].

In a nutshell, the first (basic) scenario and the second (adverse) scenario use probable (a moderate economic downgrade in Europe) then more pessimistic (macroeconomic depression without immediate recovery leap and a “W” shape economic growth) macro-economic scenarios, as well as key common assumptions and haircuts to sovereign debt instruments. “The benchmark macro-economic scenario assumes a mild recovery from the severe downturn of 2008-2009, whereas the adverse scenario assumes a “double-dip” recession. For the euro area, the GDP growth under the benchmark scenario is assumed at a level of +0.7 (2010) and +1.5% (2011), whereas under the adverse scenario the euro area would see a decrease of GDP by -0.2% in 2010 and -0.6% in 2011. For the whole European Union (EU27) the benchmark scenario assumes a +1.0% growth of GDP in 2010 and +1.7% in 2011, whereas under the adverse scenario the GDP would not grow in 2010 and would decline by -0.4% in 2011”[31]. As for the adverse scenario, on aggregate, it fakes a three percentage point deviation of GDP for the EU compared to the benchmark scenario.

Finally, in addition to a global confidence shock (which affects demand globally), the last scenario suggests an “EU-specific shock to the yield-curve, originating from a postulated aggravation of the sovereign debt crisis”[32]. The sovereign risk shock in the EU “represents a deterioration of market conditions of a similar magnitude as observed at the peak of the Greek crisis in early May 2010”[33]. It departs from adverse scenario’s parameters and reflects market’s rumors on sovereign debt in the euro zone and banks’ exposure to most fragile member states[34]. Such hypothesis are those of a shock on sovereign debts owned by banks in their trading books and on their exposure to private equity (i.e. on the private sector), which belong in their banking book.

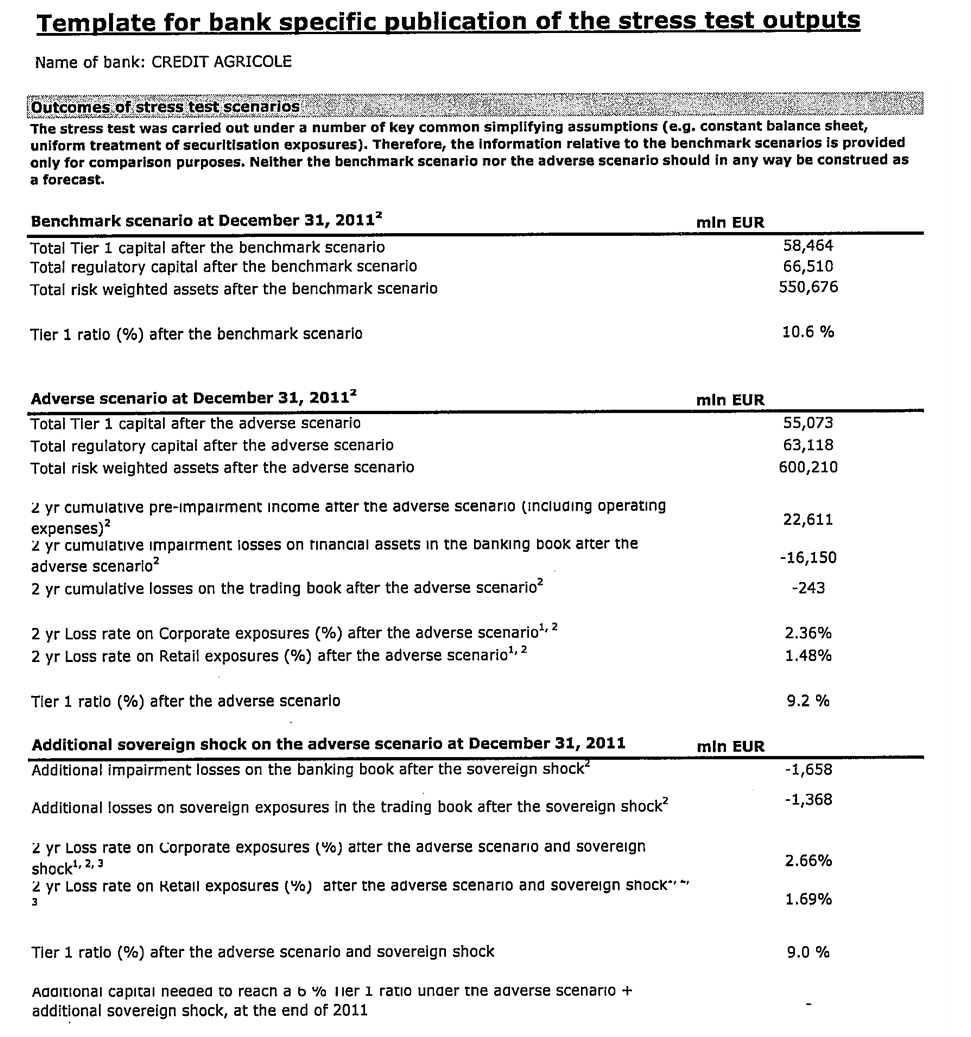

The test revealed, under the adverse scenario, a total shortfall of 3.5 Billion Euros of Tier 1 own funds and also that seven banks’ their Tier 1 capital ratios fall below 6%, which was the threshold used as benchmark for these test (without relevance to the Capital Requirement Directive II, which sets a Tier 1 capital ratio to 4%)[35]. Despite Germany, all banks of member states revealed the results, including their exposure to sovereign debts. The four French banks passed the test, far above the required 6%. All results are public and made available by each national regulators and by CEBS. For example, Crédit Agricole passed the test with flying colors, according to the following information:

{kind=link}

In the words of Victor Constancio, vice president of the European Central Bank, “toute l’information dont ont besoin les marchés pour se faire leur jugement est là: nous sommes transparents”[36]. Although very few suggest that ECB and CEBS’s transparency isn’t genuine, regulators still need to face certain critics especially regarding the methods chosen to conduct these test.

III) Did stress tests meet regulatory expectations?

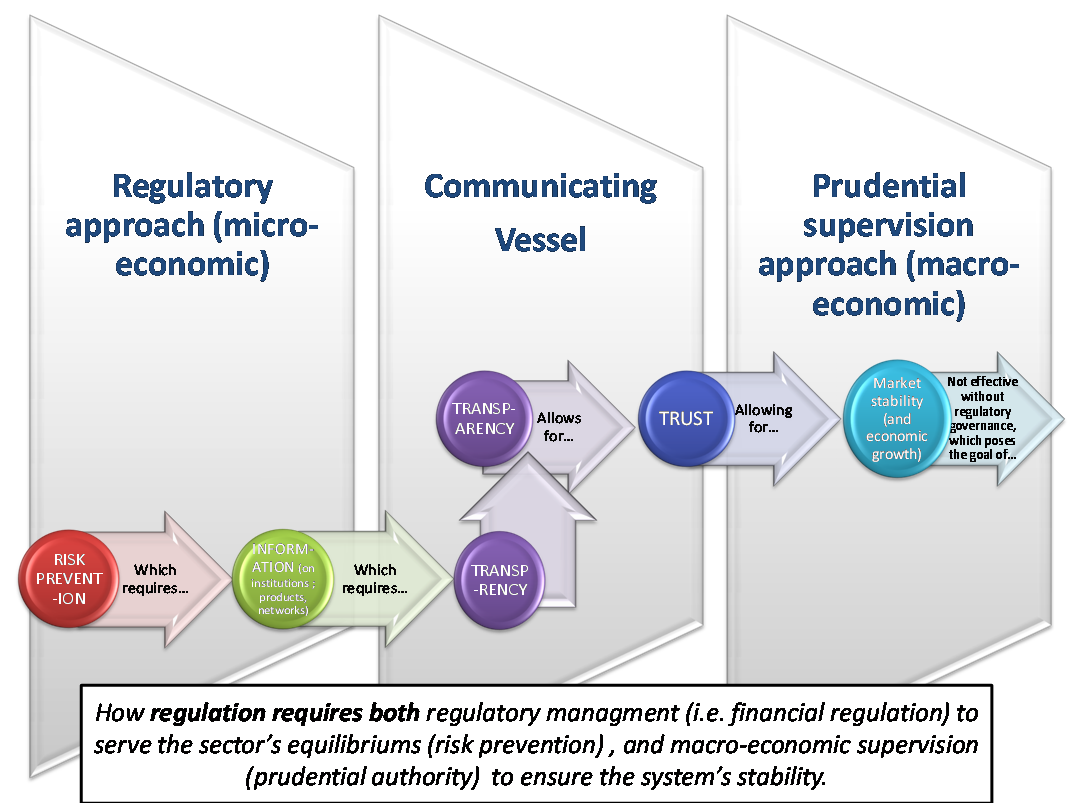

When it comes to assessing whether the tests were also a success in terms of better market regulation and stability, it seems that two types of reactions must be distinguished: economists, more focused on analyzing the health of the system itself, mainly judged these tests on their content and internal information given out (A), whereas markets focused on the act alone of communicating on these results (B). This means that, from a regulatory standpoint (i.e. reaching a specific goal to maintain certain equilibriums on a specific economic sector), tests are a success, since what primarily matters is the market’s reaction (calm vs. panic). But from a prudential point of view (more focused on macro-economic supervision of market stability), the critics made towards the quality of the information delivered (due to the selected methods and items tested) put in question the tests’ overall success. The tests’ outcome on prudential supervision is even more important that regulation must no longer be considered as solely focusing on regulatory mechanisms but also encompasses prudential supervision. They must be regarded as complementary to one another in order to ensure the overall stability of markets (C).

A) Analysts and economists reactions

In the view of national and international institutions, the publication of the results of European supervisory bank stress tests were welcomed and considered as “a major undertaking and represent an import step toward improving transparency and bolstering market confidence. The publication of the results and the actions that have been announced to address bank capital deficiencies promise to significantly strengthen the European financial system”[37]. Therefore, it works alongside other measures taken in Europe to restore market stability and risk management (such as the establishment of the European Financial Stability Facility (EFSF) and the recent and forthcoming improvement in the economic governance and financial supervisory framework within the European Union, agreed on 2 September 2010). French Minister of the Economy and French Central Bank governor also showed the same enthusiasm towards such tests.

For economists, these tests were worth the wait, since their assessment of bank solvency in times of economic deflation is in theory a huge step on its own. Economists, contrarily to financial analysts (see below), focus on the bigger picture: “the real value of these tests lies in the enhanced market transparency that comes along – the same transparency that European so far refused to implement, leading markets to believe the European banking system had something to hide”[38]. The very detailed information given out to markets is basically sufficient for analysts to pursue their own evaluation of the European banking sector. For example, Goldman Sachs immediately conducted similar tests but under different economic hypothesis. As for JP Morgan Chase, who accused CEBS of having selected far too optimistic scenarios, it also performed its own tests[39]. Still, even under more demanding capital requirement ratio or the actual taking into account of a true sovereign risk (i.e. sovereign default, such as Greece’s default), the results of these privately conducted tests are still not alarming and merely show that few more banks would have failed the test and would have needed to recapitalize in part, yet in reasonable proportions.

But analysts as well as some economists did jump on several details that could have hindered the credibility of the tests. Indeed, out of 91 banks tested, only 7 failed where markets were expecting to see at least 10 of them failing, and much more than merely 3,5 billion Euros in capital to raise in order for these 7 banks to be in adequacy with the 6% ratio imposed on by CEBS. Economists however like to be precise: financial analysts have complained that the macro-economic scenarios selected for the tests were not pessimistic enough, which is, accordingly to Jean-Pisani Ferry (one of the eight economists who called in 2009 on transparent European tests), is not correct. However, what seems to be a true problem is that tests resorted to “une définition trop laxiste de la solvabilité ou une prise en compte seulement partielle des risques sur les titres d’Etat (techniquement, seul le risque de dépréciation de leur valeur de marché a été pris en compte, pas celui d’un défaut technique) »[40].

More specifically as special Adviser and Secretary General on Financial Markets to the OECD[41] Adrian Blundell-Wignall demonstrated, tests’ flaws are mainly twofold: first no real sovereign risk is taken into account and the mere sovereign risks actually considered in scenarios are only those held by banks in their trading books, ignoring those, much more numerous, held in their banking books[42]. Therefore, when only bank’s trading book are taken into account, the EU-wide loss from the haircut applied to trading books is around 26.4 Billion Euros (the contribution of Greece, Portugal, Ireland, Italy and Spain is only of 14.4 Billion). But when banking book are taken into account, in which sovereign exposure is much more important than those present in banks’ trading book, the same haircuts applied to such exposures reveal a loss of 139 billion Euros (and haircuts applied to the five above mentioned countries amount to 75.8 billion in the banking book and 90.2 billion when including the trading book amount)[43]. Lacunas pointed out by the OECD show tremendous quantitative difference between the two methods, even though commentators admit the following: first, banking books, which are held for a long term, overpass the timeframe (2 years) chosen for the test and therefore were rightfully not taken into account under such circumstances (it remains to be seen though whether in 2 years, market focus countries such as Greece will have regain some economic growth or not), and second, it would have been politically impossible for regulators to explain why they chose and under which parameters to include a true sovereign default.

But excluding banking books from the equation is not what regulators are most criticized on. The Wall Street Journal, which also pointed many flaws in these tests although not as quantitatively alarming as the OECD’s, expressed certain concerns politically more troubling in terms of supervision (which aims at imposing transparency in order to get information) and regulation (which aims at preventing risk). Indeed, according to the Wall Street Journal (see edition of September 7, 2010), it was the regulators themselves who, by giving out accounting orders and instructions, encouraged banks to not be totally transparent[44]. For example, Adrian Blundell-Wingall agrees with the Wall Street Journal that « la donnée prise en compte aurait été la différence entre les positions de long terme et les positions de court terme, soit des données nettes et non brutes[45] ». He adds, « C’est à l’encontre des normes IFRS (International Reporting Strandards) qui sont celles habituellement utilisées en Europe. Or c’est la responsabilité des gouvernements et des régulateurs de garantir la transparence. C’est un point très important. Le manque de transparence est une très mauvaise politique car elle entraine de mauvaises décisions d’investissement. Les investisseurs sont censés, par leurs décisions, favoriser les établissements qui ont une bonne gouvernance en les choisissant. Mais ce mécanisme ne peut fonctionner s’ils ne disposent pas des bonnes données, s’ils sont trompés par une mauvaise information »[46]. Devil is in the details, and it appears that when defragmenting these tests, the sought out transparency might be jammed. Such findings clearly undermine the tests’ primary goal (reassuring investors and bankers on the EU’s financial system stability). "That would certainly be unhelpful to people's perceptions" of the tests' credibility, said UBS banking analyst Alastair Ryan. Reducing banks' reported holdings of government debt "was clearly helpful for the thing [regulators] were trying to achieve: convincing you that there's not a problem[47]" (see below).

And because transparency and homogeneity is the prime objective of the exercise, economists as well as analysts both deplore that German banks did not completely disclose the information on their own funds (especially in regards to their exposure to sovereign debt), whereas Spain played the transparency card all the way. Such a problem would not have occurred if, despite using common economic scenarios, first the control of results homogeneity would have been increased, and second, the bank-by-bank evaluation would have been exclusively carried on by the European regulator rather than by national supervisors, who had to be torn between their duty to tell the truth and their incentive to prove that their banking sector is healthy.

B) Markets’ reaction

But isn’t it the public’s reaction that matters the most for such an exercise which primarily aims at masquerading as communication exercise?

Theoretically speaking, as already explained above, the main goal is to resolve investor’s main trust issue at a specific time (in spring 2010, the European system was threaten by bank’s exposure to sovereign debt which had recently become market’s main focus). Technically, the expected positive effect on markets was principally due to the level of details announced, and should provoke several improvements such as the following: in the words of Eric Chaney, Axa’s chief economist, “les tests devraient avoir une effet sur le secteur bancaire –sans doute légèrement bénéfique- en créant davantgae de différenciation entre les banques, à la fois sur l’évolution de leur cours boursier et de leur CDS (« credit default swap »). L’exercice devrait aussi réduire certains spreads de crédit souverain [écarts de taux entre les pays, NDLR]. Sur le front des bourses, il faudra attendre que les détails des tests soient bien digérés par les investisseurs pour dégager une tendance, mais le plus probable est qu’il s’agisse déjà d’une nouvelle ancienne. Enfin, ils pourraient être positifs pour le marché interbancaire et permettre à l’Eonia, le taux au jour le jour de la zone euro, de se stabiliser. Si ce n’est pas le cas, la Banque centrale européenne (BCE) aura les coudées plus franches pour agir sur la quantité de liquidité prêtée aux banques »[48]. Further, the only reason why their results might not have had a significant impact by the time they were published is simply because markets will have already changed focus of concern. Indeed, when asked if stock markets will be affected by these tests, Eric Chaney answers that “les stress tests enlèvent une incertitude mais sont loin d’être le catalyseur le plus important. Il y a deux mois, la crise des dettes souveraines était au centre des inquietudes, alors que, désormais, c’est la conjoncture”. This suggests that such tests are nothing less than a public relation exercise and work as long as there are focused on the right market’s concern. This is a first clue that their intention, rather than their actual content (haircuts, trading books vs. banking books etc), is what matters to investors, and therefore appear as a true regulatory mechanism as it aims at keeping market stable rather than leaving it open to instant panic and therefore systemic risk.

There are many reasons why such tests were expected to have a positive impact on markets. First of all, as George Ugeux[49] notices, such exercise is remarkable because regulators substituted themselves to credit rating agencies, the credibility of which has much suffered after the crisis. National regulators take position on their banks’ health and EU regulators (CEBS, ECB) take positions indirectly on the entire EU financial system, because they suddenly has the information to do so. It is a tremendous responsibility, even though it does not constitute a rating per se. And as many noticed a year after the American stress tests, the latter were also at the offset highly criticized and detracted as too optimistic by specialists, which did not hinder markets to welcome them as a positive sign which made them a communication success. The same phenomenon will probably occur in Europe, despite the above mentioned critics regarding their methods (see II, A).

Second, it is no surprise that the outcome of the tests had a positive impact on markets. Indeed, markets are made up of investors, which, by trading stocks and securities become temporarily owners of companies’ shares. Therefore, market volatility is linked to companies’ ability to convince investors their investment is safe and their position secured, i.e. that their share value will not be downgraded or diluted. Ultimately, these tests can have two outcomes: either the bank passes the test, either it needs to recapitalize. But, the fact that markets reacted positively to the news that no forced recapitalization will occur (at least very few) is not surprising. Indeed, any forced recapitalization, while making a bank solvent again, has an adverse effect on shareholders, i.e. investors. It is so because any capitals levied on markets (in exchange for a share of the company) lead to a transfer to the bank’s creditors (the debt becoming less risky) at the detriment of preexisting shareholders. Such phenomenon is an application of the Modigliani-Miller theory: a restructuring that reduces the probability of default increases the value of the debt (held by creditors) and thus decreases the value of the equity (held by shareholders)[50].

Finally, it should be pointed out that markets actually reacted positively to the exercise before they were even completed and published. Indeed, the most spectacular market rebound occurred a few weeks before their publication, on the day the tests’ technical content were revealed by CEBS (scenarios etc.). Therefore, even before their actual publication and at a time when information given out by CEBS was still uncertain and potentially modifiable before D-day, it appears as what truly mattered to markets was the principle itself of the exercise and the transparency it was about to bring to markets (knowing that adverse scenarios were envisaged and that all results will made public), rather than their actual outcome[51]. In this view, playing with investors’ trust is almost more important than the level of details actually given out in the end. Indeed, while it is true that financial markets actually market information, and that the financial crisis was in a way an informational crisis, there is such a thing as too much information. Indeed, while making information available is a first step towards trusted and stable markets, which stress tests provide for, the second one is to make information harmonized and comprehensible, so that investors can carry out EU-wide due diligence while not being drowned with too much information. Acknowledging that too much information can work against the goals regulation aims at is typically a post crisis trend which can be found in many worldwide new regulations. For example, the recent recast of European directive on undertakings for collective investment in transferable securities (UCITS)[52] actually aims at improving “key investor information”. Such improvement does not attempt at offering investor with more information on financial products and market participants (such as UCITS), but actually at simplifying it. Such key investor information should from now on only contain the essential elements for making investments decisions. The key investor information’s content is harmonized in order to ensure that investors are protected and have sufficient information to enter comparability assessments[53]. Therefore, even though information is the most direct and efficient way to identifying and managing risk, risk management also means preserving markets from the systemic risk created by panic. The sole information that markets are transparent may therefore be enough to satisfy such goal and it seems to suffice to restore confidence in them. In this view, trust induced by transparency is therefore a regulatory tool just as important as information itself, which remains regulator’s most efficient instrument to fight against asymmetry of information (microeconomic regulation) and to have a greater assessment of the stability of markets (macroeconomic regulation). Transparency does once again appears as financial regulation‘s main vehicle, as it links confidence to information, and, more broadly, links market growth and stability to regulatory objective such as risk management.

C) Conclusion

These stress tests therefore also demonstrate that to reach such a goal, regulation may resort to any means, both legal or para-legal. Indeed, while it is true that such tests would not have been efficient if it weren’t for the EU’s regulatory framework and network (CEBS coordinating and cooperating with national regulators; the soon to be implemented European surveillance framework, on January 1st 2011, reinforcing such cooperation on a more mandatory basis), the law also needs to accept that other means need to be adjacent to it. Regulation is about managing a specific economic sector (such as the financial system) which does not only entail rule making but also message delivering by competent authority. This is why stress tests are nothing less than tricky communication exercises. As a demonstration, it is not surprising that regulators decided to test banks’ solvency rather than their liquidity. Indeed, in order for the communication exercise to work, it had to deal with a matter that had to be a communication success. As Jean Sassus, at Raymond James, underscored : « le problème des banques européennes et américaines, c’est le problème de la liquidité et de la gestion actif/passif, pas de la solvabilité. Mais ça, il était hors de question de le tester »[54]. Would the regulators had communicated on liquidity rather than solvency, the exercise would have probably failed.

Therefore, regulator’s communication skill served well regulatory objectives, since rumors and panic threats have decreased on the matter of sovereign debt. From this standpoint, and in a regulatory perspective, communicating on transparency to restore trust does equal to risk management. But from an economic point of view, trust will probably not suffice to reboot the economy (especially as the economy in Europe is wildly depending on inter-bank market which was what States were trying to refresh). Indeed, as Ben Bernanke recently underscored, regulation and supervision (the lack of which caused the financial crisis) are the way towards managing issues linked to financial stability, rather than the American monetary policy which should not be trying to deal with risk but with economic growth and inflation[55].

All in all, the outcome of the tests is not surprising: regulator’s communication exercise worked from a regulatory stand point, but isn’t sufficient to fulfill economic growth objective which lies in the hand of politics and economists. This could make sense from a pre-crisis point of view: regulation’s goal is not the stability of the economy but the stability or equilibrium of economic markets, and therefore should participate in any way to economy’s health. But this dangerously builds a wall between regulation (mainly micro economic) and supervision (mainly macroeconomic), the first attempting to manage economic sector, the other to manage the system and its stability as a whole. The crisis revealed that the mistake had been to consider the two as independent from one another because they had their interest on separate objects. Most post-crisis regulatory measures today aim at upsetting such distinction and reconciling the two, as both microeconomics and macroeconomics participate to the system’s stability. Indeed, although both regulation’s goal (risk prevention), and supervision’ goal (economic stability and growth) are at both ends of the row, they belong to the same equation (see figure 2). Therefore, regulators took notice that even though European stress tests might have appeared as a regulatory success (the risk of systemic panic was being lured away), the economic positive outcome (mainly on inter-bank markets) was still awaited. To reconcile regulation and supervision’s objectives, the European commission demonstrated that it had taken notice of all critics that analysts had proliferated on them and that may have contributed to the shy positive outcome on the economy. On August 26, 2010 regulators of the European Union published new guidelines to render these tests more difficult[56] and especially, as Michel Barnier (European Commissioner for Internal Market and Services[57]) underscores, on a more regular basis and with more disclosure on other risks than mere sovereign ones[58].

{kind=link}

[1] CEBS, “2010 EU-wide stress testing exercise, Questions and Answers”, p1. Available at: http://stress-test.c-ebs.org/documents/QAs.pdf

[2] More specifically, the publication of these tests was also bound to put an end to rumors on European banks’ exposure to sovereign debts such as the Greek, Spanish and Portuguese ones. These three countries were at the time those which had the hardest time convincing markets of their capacity to support an important amount of debt in times of slow economic growth.

[3] « En rétablissant la confiance –envers les banques qui auront réussi les épreuves-, cette initiative devrait relancer les prêts entre banques. Le circuit est gelé depuis un mois, au point que la BCE doit elle-même l’organiser ». Anne Michel, « Les stress tests, des outils de communication pour faire taire rumeurs et fantasmes », Le monde, 19 juin 2010.

[4] The focus of the stress test is on capital adequacy; liquidity risks were not directly stress tested.

[5]Marie-Anne Frison Roche, « Considérations générales sur la confiance dans l’industrie des services financiers », in Crète, Raymonde (dir.), La confiance dans l’industrie des services financiers, coll. "Cédé", Editions Yvon Blais, Montréal 2009, p.1-25.

[6] On the notion of « trust », see Annette C. Baier, in M. Canto-Sperber (dir.), Dictionnaire d’éthique et de philosophie morale, PUF, 2001 ; see also Niklas Luhmann, Vertrauen (1973), published in English under Turst and Power, John Wiley & Sons, 1979.

[7] Marie-Anne Frison Roche, « Considérations générales sur la confiance dans l’industrie des services financiers », in Crète, Raymonde (dir.), La confiance dans l’industrie des services financiers, coll. "Cédé", Editions Yvon Blais, Montréal 2009, p.1-25.

[8] Kenneth J. Arrow, Gift and Exchanges, Philosophy and public Affairs, 1972, p.357

[9] See O.E. Williamson, « Calculativeness, Trust, and Economic Organization », Journal of Law and Economics, vol. XXXVI, Chicago, 1993; contra: A. Orléan, “La théorie économique de la confiance et ses limites”, in R. Laufer et M. Ordillard (dir.), La confiance en question, l’Harmattan, 2000, and « Sur le rôle respectif de la confiance et de l’intérêts dans la constitution de l’ordre marchand », in A qui se fier ? Confiance, interaction et théorie des jeux, Revue du MAUSS, n°4, 1994, p.17.

[10] Alain Caillé (dir.), « A qui se fier ? Confiance, interaction et théorie des jeux », 4 Revue de MAUSS, Paris, 1994.

[11] Andrew G. Haldane, “Rethinking the financial network”, Speech delivered at the Financial Student Association, Amsterdam, April 2009

[12] For example, he demonstrates that complexity and homogeneity resulted in a financial network “whose feedback effects under stress (hoarding of liabilities and fire-sales of assets) added to these fragilities – as has been found to be the case in the spread of certain diseases », p.4.

[13] Other consequences being for example that financial network’s diversity was “gradually eroded by institutions’ business and risk management strategies, making the whole system less resistant to disturbance – mirroring the fortunes of marine eco-systems whose diversity has been steadily eroded and whose susceptibility to collapse has thereby increased” p. 4.

[14] Id.

[15] « La complexité et la crise financière », Remarques introductives de Jean-Pierre Landau, sous-gouverneur de la Banque de France – June 8, 2009

[16] More specifically « The overall objective of the stress testing exercise is to provide policy information for assessing the resilience of the EU banking system to possible adverse economic developments and to assess the ability of banks in the exercise to absorb possible shocks on credit and market risks, including sovereign risks”, CEBS, op. cit.

[17] IMF, « Restoring Confidence without Harming Recovery », World Economic outlook, July 2010.

[18] Peter Bofinger, Christian de Boissieu, Daniel Cohen, Jean Pisani-Ferry, Wolfgang Franz, Christoph Schmidt, Béatrice Weder di Maurao, Wolfgang Wiegard, « Pour de vrais « stress tests » européens », Les Echos, June 10, 2009.

[19] « Les « stress tests » enlèvent une incertitude mais sont loin d’être le catalyseur le plus important », Les Echos, 26 July 2010, p.23.

[20] Marie-Anne Frison Roche, « Considérations générales sur la confiance dans l’industrie des services financiers », in Crète, Raymonde (dir.), La confiance dans l’industrie des services financiers, coll. "Cédé", Editions Yvon Blais, Montréal 2009, p.1-25.

[21] Michel Aglietta et André Orléan (dir.), La monnaie souveraine, Paris, Odile Jacob, 1998.

[22] Marie-Anne Frison Roche, « Considérations générales sur la confiance dans l’industrie des services financiers », in Crète, Raymonde (dir.), La confiance dans l’industrie des services financiers, coll. "Cédé", Editions Yvon Blais, Montréal 2009, p.1-25.

[23] 10 out of 19 banks tested had to face recapitalization, for an amount up to 74.6 billion of dollars, in order to be potentially capable of facing a new financial crisis, which would involve the devaluation of their assets. At the time, tests showed that these banks could lose 600 billion dollars between 2009 and 2010.

[24] Peter Bofinger, Christian de Boissieu, Daniel Cohen, Jean Pisani-Ferry, Wolfgang Franz, Christoph Schmidt, Béatrice Weder di Maurao, Wolfgang Wiegard, « Pour de vrais « stress tests » européens », Les Echos, June 10, 2009.

[25] Id.

[26] “In each of the 27 Member States, the sample has been built by including banks, in descending order of size, so as to cover at least 50% of the respective national banking sector, as expressed in terms of total assets. As the stress test has been conducted on the highest level of consolidation for the bank in question, the exercise also covers subsidiaries and branches of these EU banks operating in other Member States and in countries outside Europe. As a result, for the remaining 7 Member States where more than 50% of the local market was already covered through the subsidiaries of EU banks participating in the exercise, no further bank was added to the sample”. CEBS, “Aggregate outcome of the 2010 EU wide stress test exercise coordinated by CEBS in cooperation with the ECB”, 23 July 2010.

[27] CEBS, “2010 EU-wide stress testing exercise, Questions and Answers”, op. cit..

[28] A « haircut » is “a risk control measure applied to underlying assets used in reverse transactions, in which the central bank calculates the value of underlying assets as their market value reduced by a certain percentage (haircut). The Eurosystem applies valuation haircuts reflecting features of the specific assets, such as their residual maturity”. European Central Bank, “Annual Report: 2003”, ECB, Frankfurt, Glossary, 2003.

[29] CEBS, “2010 EU-wide stress testing exercise, Questions and Answers”, op. cit..

[30] N.B.: Stress tests are bound to test banks’ capital adequacy ratio rather than their liquidity ratio (or current ratio). “Capital adequacy ratio is the limit on the risk-weighted credit exposure allowed to each financial institution depending on its capital base. It is also called the Cooke ratio. From 2005, it has been replaced by the McDonough ratios or tier one and tier two ratios”. Capital adequacy ratios differs from the liquidity ratio which “measures whether the assets to be converted into cash in less than one year exceed the debts to be paid in less than one year. It is obtained by dividing current assets (less than one year) by current liabilities (due in less than one year). Current ratio above 1 is considered to be protecting the creditors from the uncertainty of the assets’ monetisation as opposed to the contractually fixed liabilities repayment schedule”. Pierre Vernimmen, Corporate Finance, Paris, Dalloz, 2011, chapter 12.

[31] CEBS, “Aggregate outcome of the 2010 EU wide stress test exercise coordinated by CEBS in cooperation with the ECB”, 23 July 2010, p.3

[32] The latter impact is differentiated across countries, taking into account their respective situation. “The haircuts are applied to the market value of bonds at the end of 2009, separately for each year. Therefore, a bond which was worth 100 at the end of 2009 and which has a haircut of 4% in 2010 and 6% in 2011 should be valued at 96 at the end of 2010 and at 94 at the end of 2010”. For example, the haircut used for Greece was, for the adverse scenario, 23,2%. CEBS, “Aggregate outcome of the 2010 EU wide stress test exercise coordinated by CEBS in cooperation with the ECB”, 23 July 2010, p. 49 and 4

[33] CEBS,” 2010 EU-wide stress testing exercise, Questions and Answers”, op. cit.

[34] “In particular, related to prevailing sovereign debt risks, a common upward shift in the yield curve was applied for each country in the EU (reaching 125 basis points for the three-month rates and 75 basis points for the 10-year rates at end-2011), supplemented with country-specific upward shocks to long-term government bond yields (overall amounting to 70 basis points at end-2011 for the euro area)”, CEBS, “Aggregate outcome of the 2010 EU wide stress test exercise coordinated by CEBS in cooperation with the ECB”, 23 July 2010, p.4

[35][35] « Tier 1 is the highest quality form of capital and so can be included without limit in a bank’s capital for regulatory purposes. Tier 2 and Tier 3 capital include features that conform less closely with the underlying principles and are therefore limited to a proportion of the Tier 1 held (…).Tier 1 should consist predominantly of ordinary shares, associated reserves and retained earnings”. Financial Services Authority (UK), “Tier 1 Capital for Banks: Update to IPRU(Banks)”, October 2002, Consultation Paper 155, p. 3. Available at: http://www.fsa.gov.uk/pubs/cp/cp155.pdf.

[36] Elsa Conesa and Nicolas Madelaine, « Les vrais « stress tests » sur les banques européennes laissées aux marchés », Les Echos, 26 July 2010.

[37] Statement by IMF Management Director Dominique Strauss-Kahn on EU-Wide Bank stress Test Results, Press Release No. 10/303, July 23, 2010.

[38] Jean Pisani-Ferry, « Le test valait bien le stress », Le Monde, August 2, 2010.

[39] For example, regarding sovereign risk, CEBS only applied a 23% haircut on Greece (i.e. the “extreme” scenario in which Greek sovereign debt would correspond to a situation in which banks would only loose 23% of the amount due to them).

[40] Jean Pisani-Ferry, « Le test valait bien le stress », Le Monde, August 2, 2010.

[42] It is important in order to understand these stress tests to know the difference between a bank’s trading book and banking book. “The trading book of a bank consists of financial assets held at fair value through profit or loss and are marked to market: bank own positioning in financial instruments for profit; the execution of trade orders from customers; market making; and positions taken to hedge other elements of the trading book. All (often longer-term) exposures that aren’t in the trading book are referred to as the banking book. The latter is usually divided between exposures to: sovereign debt; retail instruments (mortgages, consumer revolving, etc); equity; and „other‟ (mainly corporate) exposures (…). Exposures held in the banking book are in principle held to maturity, and may be carried at values which differ from what their mark-to-market value (affected by liquidity) might be in the trading book. In the case of sovereign debt, provided there are no defaults or restructurings, this would be at 100 cents in the euro. In the case of non-sovereign assets, banks will choose to carry them in the banking book, and even reclassify assets from the trading to the banking book, if they believe the value if held to maturity exceeds their mark-to-market value in the trading book”. Blundell-Wignall, A. and P. Slovik (2010), “The EU Stress Test and Sovereign Debt Exposures”, OECD Working Papers on Finance, Insurance and Private Pensions, No. 4, OECD Financial Affairs Division, www.oecd.org/daf/fin, p.6.

[43] Blundell-Wignall, A. and P. Slovik (2010), “The EU Stress Test and Sovereign Debt Exposures”, OECD Working Papers on Finance, Insurance and Private Pensions, No. 4, OECD Financial Affairs Division, www.oecd.org/daf/fin, p.7

[44] For example, as part of the test, Europe's banks were required to reveal how much “government debt from European countries they held on their balance sheets. Regulators said the figures showed banks' total holdings of that debt as of March 31. At the time, worries about banks' government-debt holdings were fanning fears about the health of Europe's banking system as a whole. Release of the bank data was considered the main benefit of the stress tests, which were widely criticized as being lenient overall”. Moreover, some “banking companies excluded bonds held by subsidiaries. France's Crédit Agricole didn't count sovereign debt held by its insurance unit. A Crédit Agricole spokeswoman said the company followed guidance from regulators. Some banks' figures also were whittled down by accounting for "short" positions they held in various countries' debt. For example, if a bank held €100 million of Greek debt and €25 million of short positions in Greek debt, the gross figure was listed as €75 million. CEBS didn't disclose that the banks were calculating the figures in that way. It was unclear how much that practice reduced the gross exposures that banks reported”. David Enrich, “Europe's Bank Stress Tests Minimized Debt Risk”, Wall Street Journal, September 7, 2010.

[45] Based on Wall Street Journal’s article: “The banks based their stress-test disclosures on a template provided by CEBS. The template asked for banks to disclose their "gross" and "net" exposures to sovereign risk in each E.U. country. Most banks' disclosures didn't define "gross" and "net" beyond saying that the latter were "net of collateral held and hedges."

[46] Le Monde, « Stress Tests : L’exposition au risque souverain est sous-estimée », September 8, 2010

[47] Wall Street Journal, op. cit.

[48] Les Echos, « Les stress tests enlèvent une incertitude, mais sont loin d’être le catalyseur le plus important », July 26, 2010.

[49] George Ugeux, “Le stress test du Trésor Américain : beaucoup de bruit pour $75 millards », Le Monde, Blog « Démystifier la finance », May 8, 2009.

[50] At the offset, “a bank manages an asset A (…). The capital structure at time 0 is debt with face value D, which needs to be repaid at time 1. Equity has book value E (see Figure 1a).

government to approve such restructuring”. IMF Staff Position note, Agustin Landier and Kenichi Ueda, “The Economics of Bank Restructuring: Understanding the Options” SPN/09/12, June 5, 2009, p.9.

[51] Les Echo, « Stress-tests bancaires : va-t-on poser les questions qui dérangent ? », July 9, 2010

[52] Directive 2009/65/EC of the European Parliament and of the Council of 13 July 2009 on the coordination of laws, regulations and administrative provisions relating to undertakings for collective investment in transferable securities (UCITS) (recast).

[53] See Margot Sève, “The EU’s Financial Services Action Plan (FSAP) takes another step towards a liberal yet regulated single market in financial services through the Directive of July 2009 on UCITS”, I-1.12, The Journal of Regulation, 2010.

[54] Les Echos, « Pour les analystes, les régulateurs ne sont pas allés assez loin », July 26, 2010.

[55] Catherine Rampell, “Lax Oversight Caused Crisis, Bernanke Says”, January 3, 2010.

[56] Le Monde, « Test de résistance des banques européennes : le « Wall Street Journal » doute de leur fiabilité », Septembre 7 2010,

[57] Le monde, « Michel Barnier veut des stress tests plus réguliers pour les banques européennes », Septembre 8, 2010.

[58] « L’information sur les risques autres que souverains est restée très insuffisante, de qualité bien inférieure à celle fournie en mai 2009 pour les tests bancaires américains ». Nicolas Véron, « Stress tests bancaires : une avancée, pas une panacée », La Tribune, August 26, 2010.

your comment