The paper suggests that the neo-realistic theory of Regulation encompasses both regulatory legal rules as well as an authoritarian supervisory monitoring of their application by market participants. Further, supervision should not merely encompass microeconomic supervision but rather integrate that financial market’s interconnectedness (finance, banking and insurance) entails a reform of its current architecture, in order to preserve from market failures the system as a whole. Regulation is transversal and should not be understood as sector-specific but rather as a governance mechanism for whole systems.

It is a first in Europe since the Commission implemented, at the turn of the millennium, its Action Plan for Financial Services (FSAP): regulation is no longer exclusively assimilated to rule making. True to the “neo-realistic” definition of regulation, the latter is “a set of mechanisms, rules, institutions, decisions and principles that allow certain sectors of the economy to grow and maintain equilibriums that they could not establish solely via their own economic strength”[1]. Indeed, supervision is not an “accessory” to rules and regulations, but rather is an imperative mechanism to complete an efficient regulatory framework.

The recent financial crisis and the analysis of its causes demonstrated that such definition tends to be more and more agreed with rather than the one classically understood by many, who deemed that regulation was only a set of legal rules (laws, directive, regulations etc.), which underscores the importance and the distinction between regulation and règlementation. Regulation as a whole, understood as a market governance method, encompasses both and is inevitably failing if both rules and supervision are not provided for by those –mainly States- who intend to implemented a regulatory structure to uphold markets’ equilibriums. This is why Jacques de Larosière, one of the most important European actor in the analysis of the financial crisis’ causes, identified the lack of supervision, or rather its inefficiency, to be the true guilty party in the crisis’ triggering and propagation.

For Jacques de Larosière, former managing director of the International Monetary Fund (IMF) and author of the European Commission’s report on European financial supervision, the reason why technical and economic occurrences (such as excess of liquidity or the American real estate bubble) were able to act as a trigger of the financial crisis is because of a more profound vulnerability: the “insuffisance flagrante de surveillance des autorités financières[2]”. His report, which was bound to become the basis for the Commission’s proposal on EU financial supervision reform, clearly states that when it comes to this regulatory issue, the problem does not lie in the absence or lack of rules and regulations but in the incapacity of regulators to monitor their respect and the overall effect of market participants’ behavior on the stability of the system. “Pour moi, les lois de cadrage des activités financiers –la régulation- ont été prises par défaut. Mais même dans ce cadre insuffisant, les autorités auraient dû agir. L’exemple caricatural en est l’américain AIG : pour échapper à l’interdiction faite aux assureurs d’avoir des activités de marché, il avait acheté un caisse d’épargne qui s’est lancée dans des opérations très complexes. Autre exemple : les subprimes, ces prêts immobiliers accordés sans garanties de ressources, qui ont gonflé hors de proportion parce qu’ils ont été revendu (titrisés) dans des conditions totalement obscures (…). La surveillance (…) reste mal perçue aux Etats-Unis et en Grande-Bretagne. Pour ces pays, régulation [in the sense of legal rules] et surveillance, c’est pareil. Pour moi, il faut les séparer et l’essentiel repose sur la surveillance, le contrôle précis des autorités, et sur l’unité et la coordination des organismes de supervision qui fait aujourd’hui cruellement défaut »[3].

Jacques de Larosière is joined in his reasoning with former American Federal Reserve governor Ben Bernanke who agrees that the crisis would not have spread is such manner if it weren’t for the obvious lack of supervision and regulatory observation and reaction. Indeed, they both agree that it was not in particular the lack of regulation (rules on certain financial products or market participants) which made the crisis that catastrophic, but the lack of intervention by regulators. The regulatory framework as it was in place before the crisis was therefore unbalanced and the true vulnerability of the system.

But analysts do not blame the institution, the idea, of sector specific regulators, as they appear as the most important communicating vessel between on the one hand legal rules, individual decisions upon market participants, agreements and registrations etc., and, on the other hand, information gathering (in order to fight against asymmetry of information), providing for a authority closer to the sector than the State (which for example allows it to impose on market participants a certain amount of transparency), and a more authoritarian institution than an authority chosen by self regulated markets (likely to be in conflicts of interest) and upholding regulation (here financial regulation) ‘s main objectives (such as risk prevention or management and consumer protection). For Larosière and Bernanke, it is this second set of powers that regulators were either unable to fulfill or were simply not in place to do so. For example, either because regulators did not get certain information (because of asymmetry of information) to foresee a real estate bubble, or because such information was too scattered between different sectors and actors or possessed but not gathered by non cooperative supervisors, or because, even if they had been able to see the bigger picture, regulators did not have sufficient mandatory powers to act on it and take urgent measures to stop certain behaviors, the framework was indeed flawed.

Larosière does not suggest to repel the idea itself of regulator because it is the guardian of ex ante mechanisms which are always preferred for global markets such as financial ones since their most important threat is systemic risk, whereas ex post powers, as efficient on market participants they can be, hardly provide for a compensation to a crisis occurrence (since ex post means that regulators intervene after a certain event occurred). In his view, when it comes to post-crisis reregulation, most efforts must be put in a stronger, more organized, more powerful supervision system, closer to economic realities (market interconnectivity, macroeconomics’ influence on microeconomics and vice versa). “the present crisis results from the complex interaction of market failures, global financial and monetary imbalances, inappropriate regulation [i.e. regulatory rules], weak supervision and poor macro-prudential oversight. It would be simplistic to believe therefore that these problems can be "resolved" just by more regulation [i.e. regulatory rules]. Nevertheless, it remains the case that good regulation is a necessary condition for the preservation of financial stability”[4].

The main message of this reasoning is not to deny that the crisis was a crisis of regulation, but that is was a crisis of regulation in the sense that regulation encompasses both legal rules and supervision, and mainly failed on this second aspect. Indeed, would the rules had been there and properly tailored to specific market situation (which they were not always), regulatory supervisory systems throughout the world probably would not have managed to stop the domino effect in time. Therefore, the crisis was not due to a lack of regulation in the sense of lacks of rules[5] (although it is obvious that sectors were that much deregulated that lack of rules, leaving open the door to self-regulation, greatly contributed to the crisis propagation) but in the sense that this it is a market governance mechanism which was only in part efficient. The crisis is a crisis of supervision, and in that indeed a crisis of regulation.

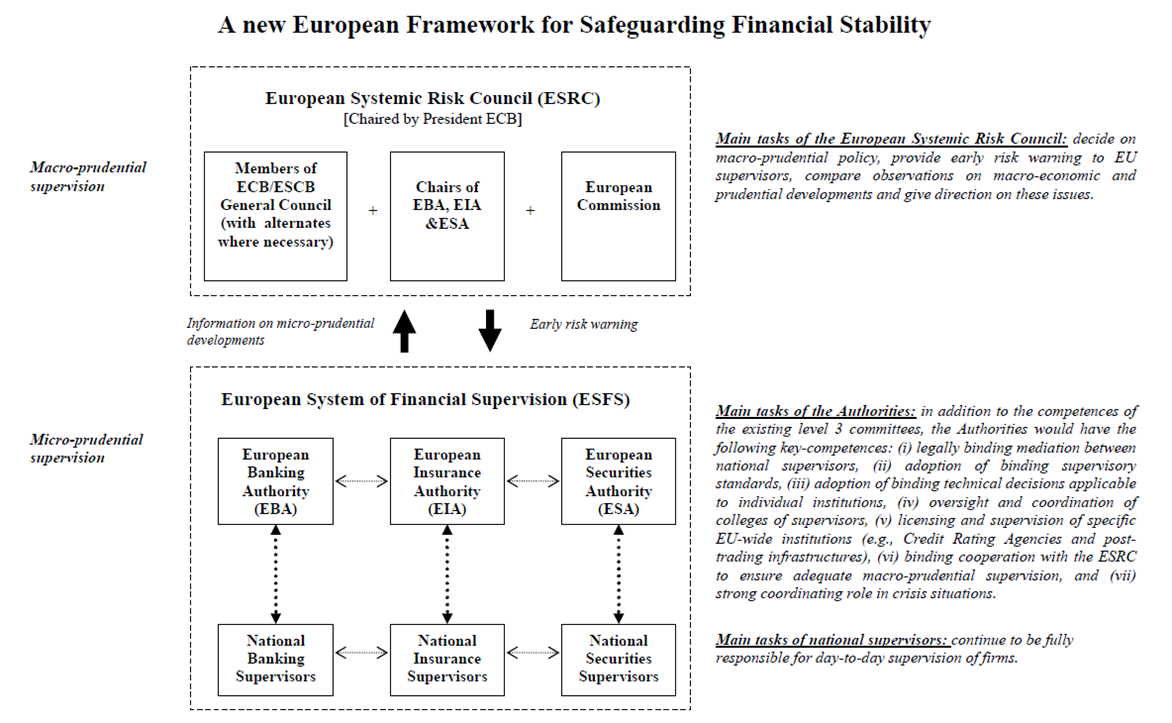

On September 2010, Europe finally showed its adhesion to such definition of regulation, as it recently voted on a new EU-wide financial supervision framework, after a year of negotiations, the subject being that critical. The Commission acknowledged that the current “arrangements for financial supervision in Europe are inadequate in an EU-wide integrated financial services market”. The European idea is to go from the current supervisory architecture, mainly based on cooperation between local regulators overseen by committees with mere advisory powers (three committees with advisory powers: the Committee of European Banking Supervisors (CEBS), the Committee of European Insurance and Occupational Pensions Committee (CEIOPS), the Committee of European Securities Regulators (CESR)), to a bipolar architecture. A first pillar based on a European system of financial supervisors (ESFS) in order to “help restore confidence; contribute to the development of a single rulebook; solve problems with cross-border firms; prevent the build-up of risks that threaten the stability of the overall financial system[6]” and a European Systemic risk Board, to ensure market stability. Behind such potential economic progresses, the main improvement of such system is twofold: first, it is no longer based on a sector-specific cooperation between national regulators under a non compulsory European supervision ; second, it takes act that regulation is trans-disciplinary and broadly encompasses categories which used to be separately considered: microeconomic vs. macroeconomic; regulatory vs. prudential rules, sector specific vs. interconnected systems.

I) The Pre-crisis European financial supervision : A defragmented microeconomic supervision framework

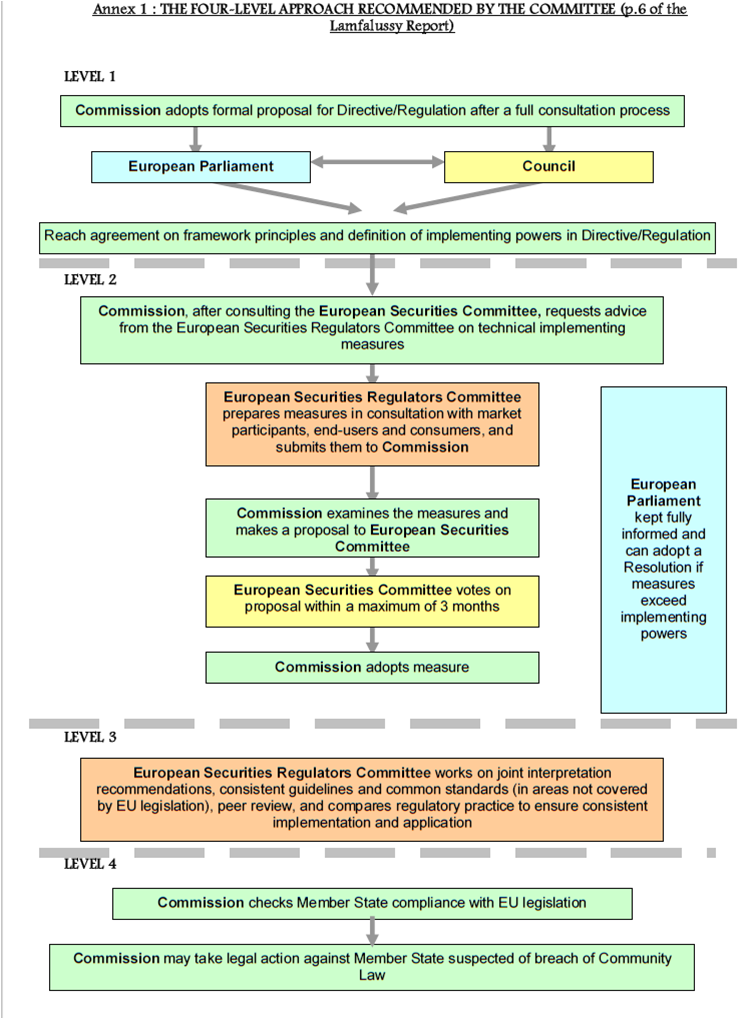

When the crisis busted, the European supervisory architecture was mainly the organizational consequence of a legislative process invented to improve the rule making on EU financial services, called the Lamfalussy process (“a four-level, comitology-based regulatory approach for adoption, implementation and enforcement of legislation and implementing measures in the financial services area[7]”). The EU architecture was made up of Committees of Supervisors, called Level 3 Committees, made up of high-level representatives from Member States' supervisory authorities, established in 2001 in securities and in 2005 in banking and insurance (the extension of the Lamfalussy process to banking and insurance was part of the EU’s effort to increase cooperation and coordination between national supervisory authorities, including crisis management). It appears a though, vaguely acting in compliance with an supra national advisory committee, the implemented architecture’s main default was that it favored cooperation between local authorities rather than centralized supervisory powers between supra-national authorities (A), which does not take into account the modern challenges of regulated markets (B).

A) Flaws streaming from mere consultative microeconomic entities

The current but soon to be changed supervisory architecture in the EU is deficient from two standpoints: from the companies’ point of view, and from the regulators’. From the companies standpoint, and at the time M. de Larosière was appointed to conduct a study on the efficiency and improvements of the EU supervisory system, firms of the European Union were still mainly submitted to the surveillance regime of their home country. Transnational companies’ affiliates incorporated in a host country were submitted to the latter’s legislation. As for their mere office branch in a host country, although they depended in theory on their home country’s legislation, host country’s authorities had their word to say, for example in case of investment services, the domain of control of the host country’s authorities being vast (for example they dispose of the right to examine their incorporation’s modalities, see article 32 of the MIFID)[8].

“This organization is a very complex one, leading to multiple reporting lines between

supervisors and supervised entities and to complex mechanisms of cooperation between home

and host supervisors. Some argue that the present arrangements should be preserved because,

in certain cases, it could be better to handle complex financial institutions with different

supervisors holding different views on a number of issues »[9]. But facts speak for themselves and the fragmentation and complexity of a supervisory system may be the cause of great dangers: for example, it was the fragmentation of the American surveillance architecture that brought AIG to fail. Indeed, the collapse of the group was provoked by a lax, state-by-state, regulatory framework for insurance, combined with the total absence of a unique regulator at the Federal level, supervising and being responsible for the national insurance industry.

Many consider that current European mechanisms, which only allow for the cooperation between home country’s regulators while leaving the Level 3 Lamfalussy Committees left with mere consultative tasks, are insufficient. « Host supervisors do not have comprehensive means to challenge the home state supervision of a group which has branching activities in its territories;

- there is no binding mediation mechanism arbitrating between home and host supervisors,

whether for banks, insurance companies or investment firms;

- if a national supervisor fails to take a necessary measure, there is no quick mechanism

allowing for a collaborative decision to be taken in relation, for example, to the liquidity

or solvency position of a group;

- there are no effective cross border crisis management arrangements »[10], which poses certain risks in regard to transnational systematically important institutions.

The consequent complexity of the regime entails that no financial stability can actually be looked out for. Moreover, the stability of the system and States themselves depend exclusively on their local regulator’s efficiency. One regulator’s supervisory mistake or absence can have dramatic consequences for the internal market, which is the world’s number one financial market. Moreover, the costs entailed by the numerous yet different regulators’ position and of their divergent level of requirements (for example in regard to requirements on information, transparency etc.) are ever increasing, counter-productive and anti-incentives. This is especially a problem for transnational companies which have to report to several different authorities, which may also have diverging opinions on regulatory and supervisory issues, and put companies in a position in which they need to comply to different injunctions (such system also posing problems in terms of regulatory competition).

From an administrative point of view, the Lamfalussy process greatly contributed to the improvement of the EU’s legal framework and set of rules on regulatory matters. Indeed, it allowed for the creation of good quality framework and mechanisms, thanks to its decision making process based on the Level 3 Committees’ technical expertise, public consultation and decisionnary transparency. However, the most obvious flaw of the process was that it did not deal with prudential supervision[11], only technical consultation on drafting and implementation of EU law. The purpose of the process was to help converge Member States’ supervisory practices and interpretations, and contribute to harmonizing EU-wide regulatory rules and practices eventually supplemented with non-mandatory guidelines. As for the Level 3 Committees’ accessory tasks, the Larosière’s report underlines that the aim to converge supervisory practices, agree on common day to day interpretations and applications of EU rules with non-binding guidelines, and foster greater trust among supervisors, “have proven to be very difficult. Without recourse to qualified majority decision making until very recently, and without legal powers the Level 3 committees have been unable to converge their activities sufficiently. Some of this is due to the fact that some directives in levels 1 / 2 of the Lamfalussy process allowed for optionality and gold plating – so level 3 could not resolve the problems left over from levels 1 and 2. But in other cases, national supervisors did not cooperate sufficiently to converge either supervisory practices or interpretations – whether the reason is to protect a national champion, restrict competition, preserve a national practice viewed as a competitive supervisory or regulatory advantage or just sheer bureaucratic inertia”. Ideally, the Level 3 Committees should have been able for example to propose common and harmonized reporting formats, or agree on clearing and settlement standards (agreement between the Committee of European Securities regulators and the European System of Central Banks). As for panaeuropean institutions which highly demanded to be looked out for such as credit rating agencies, no authority such as the Committee of European Securities regulators had the legal power to either supervise or coordinate their registration (which was, until Regulation of September 16th 2009, done at the national level).

In a nutshell, the Lamfalussy process, which indeed did not encompass rules on how to not only legislate on regulatory rules but also on how to supervise their application by members states or market participants in general, however counted on its third and fourth steps, mainly relying on the work and effort of its Level 3 Committees, to see such legislation correctly and harmonizingly applied in all Member States. In such view, regulation does depend on both regulatory rules but also on their supervision when it comes to implement them and having them respected.

In this view, the process could not be hundred percent successful if two of its four steps could not be properly achieved. This is the reason why, already in 2007, when it became obvious that a part of the process was not efficient, analysts suggested the following recommendation for its improvement, for example on the issue of prudential norms: “La mise en place d’une interface prudentielle rationalisée et de conditions de concurrence équitables pour les intervenants de marché ainsi que la nécessité d’un suivi adéquat et d’une réponse rapide aux risques transfrontières potentiels impliquent des mesures efficaces à différents niveaux du processus réglementaire et prudentiel de l’UE. En particulier, la convergence et la coopération prudentielles transfrontières ne seront suffisamment renforcées que si des progrès effectifs sont réalisés à chacune des quatre étapes suivantes ; Premièrement, les organes communautaires concernés (…) doivent fournir un cadre institutionnel efficace ainsi qu’une impulsion et une orientation politiques pour la poursuite de la convergence et de la coopération transfrontières au sein du dispositif Lamfalussy. • Deuxièmement, les directives de l’UE et les mesures d’exécution favorisant une convergence plus étroite des règles nationales et améliorant le cadre réglementaire pour la coopération transfrontière doivent être adoptées et effectivement appliquées par les États membres. Ces travaux se rapportent aux niveaux 1, 2 et 4 du processus Lamfalussy. • Troisièmement, des règles renforcées au niveau de l’UE doivent être mises en œuvre sous la forme d’une convergence étroite des exigences prudentielles. En vue d’atteindre cet objectif, les contrôleurs de l’UE doivent convenir d’orientations communes pour la transposition au niveau national de directives et de mesures d’exécution européennes et en surveiller le respect. Pour le secteur bancaire, ces travaux sont effectués au Niveau 3 du processus Lamfalussy avec le soutien du Comité européen des contrôleurs bancaires (CECB). • Enfin, des exigences prudentielles communes doivent se traduire par une cohérence dans les processus prudentiels courants. Ces travaux plus opérationnels, réalisés par les autorités nationales compétentes, sont également soutenus par le processus de Niveau 3 et les activités correspondantes du CECB »[12].

As we will see below amongst Larosière’s recommendation, the French Central Bank, in 2007, was also already suggesting, in order to move faster towards the convergence of prudential requirements, to reinforce the role and of Level 3 Committees’ role and functions (in the case of the Central bank’s interest, the CEBS). Specifically, “l’amélioration des mécanismes de prise de décision du CECB, comme, par exemple, un recours accru au vote

à la majorité, pourrait compléter efficacement les mesures précédemment mentionnées pour renforcer le statut institutionnel du CECB au niveau de l’UE et au niveau national. Le vote à la majorité, déjà possible s’agissant des avis formulés par le CECB sur les règles de Niveau 2, doit également être envisagé pour l’adoption des produits de Niveau 3 dans les cas où des avancées concrètes ne peuvent être réalisées sur la base d’un consensus. L’introduction d’un vote à la majorité pour les produits de Niveau 3, qui nécessiterait une modification de la charte du CECB, n’aurait aucune incidence sur leur nature juridiquement non contraignante. Pour assurer la mise en œuvre efficace des décisions majoritaires dans le cadre du CECB, qui fonctionne sur une base volontaire, il serait utile que les membres du comité s’engagent à observer les décisions prises à la majorité suivant le principe « se conformer ou s’expliquer». We will see below how such recommendation were in fact transposed into the reform.

For all these reasons, and because a process which aims at elaborating appropriated rules to technical situation can only be efficient if supervision is also insured, the Larosière report concludes that “against this background, the Group considers that it is crucial that in the future EU supervisors exercise their competences in a more effective, collaborative and coordinated way than today. The existing level 3 committees have clearly reached their limits in terms of informal cooperation methods. ».

B) What the crisis market failures say on supervisory flaws

Although the crisis acted as a trigger to amend and reform the European supervisory architecture, the fact that the latter was failing wasn’t news to the Commission: for example, in 2008, the European Commission had already launched a consultation on possible amendments to Commission Decisions establishing the Committee of European Securities Regulators (CESR), the Committee of European Banking Supervisors (CEBS) and the Committee of European Insurance and Occupational Pensions Supervisors (CEIOPS)[13]. “The overall objective is to align, clarify and strengthen the responsibilities of the Committees of Supervisors and to ensure their contribution to supervisory cooperation and convergence at EU level, and to the safeguarding of financial stability”[14].

The reason why the Commission was already suspicious about the efficiency of the EU supervision was because, when it launched its “Financial Services Action Plan” and appointed to do so a committee of Wise men in 2001, chaired by Alessandro Lamfalussy, on the regulation in Europe of financial services, it did not mandate the latter to express itself on the issue of financial services supervision and stability. Moreover, although the Committee of Wise men had excluded the question of prudential supervision as it was not mandated to study it, and although it specifically identified the current supervisory structure as being Europe’s weak spot, the political will to reform the financial services supervisory system was at the time inexistent. In the words of the Committee of Wise men: “the Committee believes that there is an urgent need to strengthen cooperation at the European level between financial market regulators and the institutions in charge of micro and macro prudential supervision [15]». Encouraged by the Lamfalussy process and its three Level 3 Committees, Europe’s supervision was fragmented and based on mere cooperation between national authorities, even though the regional financial services market had become real, if not absolutely global.

Jacques de Larosière was therefore invited by the Commission in October 2008 to create a group of experts (the High-Level Expert Group on financial supervision in the EU) in order to submit the schematics of what a more solid European supervision of the financial industry could look like. Its first mission was to identify which of the crisis’ causes were being rooted into lack of or lax supervision. Indeed, by identifying the crisis causes, M. de Larosière was be able to submit a proposal for reforming Europe’s financial supervision into an architecture more apt at fulfilling regulatory goals such as market stability, risk prevention or consumer protection.

First of all, the Larosière report blames the lack of macroeconomic supervision, especially in regards to liquidity. Indeed, during years preceding the crisis, certain macroeconomic conditions characterized by a tremendous increase of liquidity and exceptionally low rates stimulated the developing of new financial products with higher profitability than regular assets. An important change in business models, turning to short term investments induced by pro-cyclical accountability and prudential rules, started to occur. “In fact, the business model of US-type investment banks and the way they expanded was not really challenged by supervisors and standard setters”[16]. Such business models, pushed towards short term benefits, such as, inter alia, the “originate to distribute” banking model, combined with new financial practices such as securitization, allowed for the fading of apparent risk on markets, thereafter hidden and spread around the world thanks to financial markets’ globalization[17].

To had been able to foresee the crisis would have meant that regulators should have been more focused on liquidity of markets, and paid more attention to the impact of disparate (in appearance) events on sectors or markets as a whole rather than exclusive focus on each individual firm, since such aggregated events on various markets (banking, insurance, financial) highly participated to the developing problems.

Second, a failure of interregulation clearly occurred, since none of insolated problems on each specific markets were communicated between regulators in time before they spread on to other markets. For example, “while US supervisors should have been able to identify (and prevent) the marked deterioration in mortgage lending standards and intervene accordingly, EU supervisors had a more difficult task in assessing the extent to which exposure to subprime risk had seeped into EU-based financial institutions. Nevertheless, they failed to spot the degree to which a number of EU financial institutions had accumulated – often in off balance-sheet constructions- exceptionally high exposure to highly complex, later to become illiquid financial assets[18]”. The amount of asymmetry of information was tremendous not only in market participants vs. regulator relationship, but also between regulators themselves. Regulators’ capacity (central banks, supervisors, market participants etc.) to take action and act in a timely yet harmonized manner was also put off by the lack of supervisory organization.

As the Larosière report puts it: “taken together, these developments led over time to opacity and a lack of transparency. This points to serious limitations in the existing supervisory framework globally, both in a national and cross-border context. It suggests that financial supervisors frequently did not have and in some cases did not insist in getting, or received too late, all the relevant information on the global magnitude of the excess leveraging; that they did not fully understand or evaluate the size of the risks; and that they did not seem to share their information properly with their counterparts in other Member States or with the US”.

Further, the impact of issues such as regulators’ resources (budget, task force etc.)[19] and their education/skill must not be underestimated, as well as the too often major gaps from one country to another when it comes to their supervisory policy (often due to regulatory competition which induces regulator not to take action against financial institutions).

Finally, a major issue lies not only in the exclusively microeconomic focus of regulators rather than combined to a macroeconomic one, but also in the total absence of mechanisms of crisis management (without common crisis management framework, States had to act timely yet uncoordinatedly to avoid banks’ failures). Therefore, any lack of supervision allowing for the crisis was worsen by the fact that no regulatory response could be provided due to the absence of such crisis management infrastructure (which would have helped States, market participants and regulators to cooperate more efficiently).

In a nutshell, “l’ampleur de la crise qui a frappe l’Europe était principalement due à l’inadéquation des structures de supervision européennes, décentralisées et fragmentées, fondées sur des mécanismes de coopération entres autorités nationales, face à un marché unique des services financiers. Bien que perfectibles, les règles de fonds qui constituaient le cadre réglementaire européen au moment de la survenance de la crise financière n’étaient pas fondamentalement inadaptées. Si un changement de cap s’impose, c’est donc essentiellement au niveau des structures de supervision [20]».

Based on these premises, mainly acknowledging that micro does not go without macro, that risk management entails observing more than one sector specific market (including risk of liquidity), and that both ex ante and ex post mechanisms must be provided for (such as crisis prevention but also crisis management), the Larosière report incorporated its findings into its reform proposal for a new European supervisory architecture.

II) Towards a vertical supervisory architecture for global and interconnected markets

The Larosière report acknowledges that regulation encompasses both the need for solid rules bound to reestablish financial stability, prevent risk and protect consumers, and the crucial necessity to reform the financial system of supervision (the process designed to oversee financial institutions in order to ensure that rules and standards are properly applied)[21]. Regulatory rules “and supervision are interdependent: competent supervision cannot make good failures in financial regulatory policy; but without competent and well designed supervision good regulatory policies will be ineffective. High standards in both are therefore required”[22]. The Larosière report was therefore divided between measures regarding regulatory rules, and regulatory supervision, itself subdivided in two aspects: a first step aiming at reforming Europe’s supervisory architecture, and a second needed to implement a European crisis management mechanism. “Cependant, rien n’est moins simple que de reformer des règles de supervision du marché qui, limitées par le principe de subsidiarité du Traité et basées sur la coopération international, touchent à la souveraineté des Etats membres. La tentation pourrait être grande pour le monde politique (…) de faire passer au second plan la nécessaire –mais délicate- réforme des structures de supervision »[23].

Such fear is not totally unfounded. Indeed, while the Commission’s legislative proposal mainly duplicated the report’s main ideas, such as the create of a two faced regulatory European supervisory framework (one macroeconomic institution for systemic risk management, the other regrouping micro economic supervisory European and national institutions), its proposal was highly influenced by a number of Member States (such as the UK; with large financial centers) which were in favor of a limited reform approach. The political tension and the differences of approach between the Parliament, in favor of a true reform, and the Council, more willing to protect State’s sovereignty, “led to a significant reduction in the scope of the Commission proposals, themselves considered by the EP as not going far enough. Parliament's rapporteurs from the beginning argued that the system needed serious reform so that risk would be better understood, primarily through much improved communication between national supervisors”[24].

The main differences between the Commission’s proposal, attentive to member states’ opinion, and the Parliaments’ reform, which finally made its way through on September 22nd 2010, lies in the encompassing scope of the Larosière reform. Indeed, beyond the main architecture suggested by the report (B), it also recommends that new authorities have a true regulatory and mandatory powers, in order to implement certain innovations that supervision need to undergo in order to properly fulfill its mission of risk prevention and market stability (A).

A) New transversal regulatory principles…

One of the most pregnant reform of the EU supervision system takes into account the too long dichotomy between macroeconomics and microeconomics. Classic supervision usually tended to stay focused on microeconomics, i.e. on the surveillance of market participants rather than the system itself. But the fact that the entire financial system may be exposed to similar risks are even identical ones was not sufficiently taken into account. Macroprudential supervision permits for example to prevent the risk of contamination subsequent to the failing of an institution. Indeed, because such institution, considered as “too big to fail”, were systemically important[25], their default could not only contaminate to entire system but also create other negative externalities, such as the loss of confidence on interregulated global markets. The point of macroprudential supervision is to limit some of the financial sector’s difficulties in order to protect the “real” economy from important loss of “real” goods. “Macro-prudential analysis therefore must pay particular attention to common or correlated shocks and to shocks to those parts of the financial system that trigger contagious knock-on or feedback effects”[26].

In this view, macroprudential supervision and microprudential supervision are linked, since they both feed off the others’ data in order to both contributing to market stability (microprudential information feeds macroprudential analysis which contributes to microprudential efficiency). The new EU-wide supervision will need to be as much focused on market participants than on the system in its entirety.

Such observation forces to take into account another side of regulatory supervision, which is that the latter must not focus on one specific sector but rather under the system in all of its complexity. And because the financial sector is no more composed of mere financial markets but is made up of banking and well as insurance and well as financial markets, then macro prudential supervision must take a hold of this economic reality and encompass all of finance’s sectors, rather than being limited to banks. Such macro prudential supervision must take into account this complex economic system, in the way that it has become cross sectoral but also in that the sectors under study are global rather than national. Most importantly, such supervision will not be efficient if no supra national assessment or judgments may be taken by an authoritarian entity on macro prudential risk (rather than mere national decisions and monitoring).

This is the reason why, as we will elaborate on below, the report suggested to create a regional authority in charge of watching out for market stability, assessing macrofinancial risk (in order for national regulators to take it into account), and capable of alerting authorities if it deems necessary. In order to fulfill its role, it would need all the cooperation and information national regulators have and can give. The mission of such a systemic risk council would be to pass judgment on risk, publish recommendation on macroprudential policies, warn the proper authorities if risk arise, and compare national and supra national information on macroeconomic and prudential evolution.

While the current entity best capable of detecting and assessing macroeconomic risk is the European central bank, the latter could not achieve such purposes without the total contribution of national and supra national sector specific regulators. Because transparency and symmetric information is the key to a stable system, such systemic risk entity would need to welcome all central banks as well as representative of national regulators and of the three European sector-specific regulators (Level 3 Committees, also bound to be transformed by the reform into true authorities). Beyond the mere presence of such sector specific regulators and of all European governors of central banks, such entity in charge of systemic risk will need to be provided with constant information, exchanged between national supervisory authorities and itself, in order to reach total transparency of market information and therefore have a better perception on sector-localization, quantity and retainers of financial risks.

Such entity is therefore a true example of how regulators are primarily ex ante mechanisms to sustain markets’ equilibrium. “L’objectif premier de la surveillance est de faire en sorte que les règles applicables au secteur financier soient mises en oeuvre correctement afin de préserver la stabilité financière et, partant, de maintenir la confiance dans le système financier dans son ensemble et de garantir une protection suffisante des clients des services financiers. Une fonction des autorités de surveillance est de détecter les problèmes à un stade précoce afin d’empêcher la survenance de crises ». This is the reason why it is crucial that such a systemic risk manager can at all time inform and urge authorities to take significant measures (either political or legislative) on any sign of market failures, and that be implemented an “effective and enforceable mechanism to check that the risks identified by the macro-prudential analysis have resulted in specific action by the new European Authorities (see below) and national supervisors”[27].

But the crisis does not teach that macroprudential supervision is suddenly more important than microprudential, but rather that they must work together: without a solid network of microeconomic supervision, macroeconomic effort may be in vain. Yet the regulatory microeconomic mechanisms in place (the Lamfalussy Level 3 Committees) “are not sufficient to ensure financial stability in the EU and all its Member States. Although the level 3 committees have contributed significantly to the process of European financial integration, there are a number of inefficiencies which can no longer be dealt with within their present legal structure (i.e. as advisory bodies to the Commission)[28] ». Such entities were far away from being true sector-specific regulators as they did not have any “authority” per se on the sector they were suppose to monitor. In order to improve the regulatory environment, such authorities should have more important basis and, while working on each of their assigned sector, work together for the protection of the system as a whole to which their specific sector belong, i.e. the European Financial System, encompassing banking, financial markets and insurance. Such a supra national regulator could encompass for each sector an integrated network in which national regulators would work in cooperation with reinforced level 3 entities. Such a bottom up approach is in total adequation with regulatory law’s principles. Indeed, national entities must go on with their regulatory prerogative since they are more familiar with their own national markets and have direct authority (figuratively and strictly speaking) over national market participants. This takes into account the fact that regulation is above all very technical, at least as technical as its object is. Therefore in sectors such as finance, banking or insurance, the need for technocratic monitoring is crucial, as well as the feeling that a certain authoritarian shadow is planning over markets. On the other hand, choosing to keep national rules and supervision jurisdiction puts regulation faced with the dilemma of global markets versus mere national sovereignty to act upon them. Because most systematically important institutions are nowadays transnational, they need a supra national supervision. For example, “the present processes and practices for challenging the decisions of a national supervisor have proven to be inadequate; for example the embryonic peer review arrangements being developed within the level 3 committees proved ineffective. At present (and until any practical arrangements for supervision on an EU basis are both agreed in principle and translated into practice), extensive reliance is and will be placed on the judgments and decisions of the home supervisor”. And in the case when “a financial institution spreads its activities into countries other than its home base by branching from its home country (…) an effective means of challenging the decisions of the home regulator is needed”[29]. Therefore, keeping and actually reinforcing Level 3 Committees (transformed into true “authorities”) is necessary in order for them to handle issues which by definition overcome Member States’ sovereignty yet pose the most probable risk to the system. Where national regulators lose jurisdiction over certain entities which are transnational, or where national entity cannot edict and impose their regulatory rules on other member states’ regulators, supra national authority, conferred with true normative power to define and coordinate supervisory norms (and harmonized supervisory policies), could make sure national entity all work in the view of cooperation and in the view of protecting such common good that is the European financial system. But when the stability of the European financial system becomes a universal priority, it requires that its supervisory body be independent, safe from political or lobbying capture, powerful (with mandatory powers, allowing them to harmonize supervisory rules or take concerted and mandatory decisions in urgent cases) and, just as any other regulator, must be accountable for its actions and framed by a sort of check and balance mechanism[30].

Such a bicephalous structure, with one entity in charge of monitoring risk and insuring market stability as a whole system (putting under the same umbrella supervision of both banking, financial and insurance sectors), the other in charge of insuring that market participant are solid and well behaved, provides for the reconciliation between a macroprudential and microprudential supervision, and takes into account the interconnectedness of markets. “The Unionmacro-prudential oversight of the financial system is an integral part of the overall new supervisory arrangements in the Union as the macro-prudential aspect is closely linked to the micro-prudential supervisory tasks attributed to the ESAs. Only with arrangements in place that properly acknowledge the interdependence between micro- and macro-prudential risks can all stakeholders have sufficient confidence to engage in cross-border financial activities. The ESRB should monitor and assess risks to financial stability arising from developments that can impact on a sectoral level or at the level of the financial system as a whole”[31]. Such cross-sectoral and closer to the reality risk organization is very close to what the doctrine has been prescribing ever since the crisis. As Marie-Anne Frison-Roche underscores, on the subject of the French Autorité du Controle Prudentiel (an entity which recently merged the insurance and the banking regulatory supervision in France, with close collaboration with the financial market regulator) and which is about to be coupled with the creation of a French systemic risk council: “ce régulateur est spécifique parce qu’il dépasse la summa divisio que l’on posait naguère entre la surveillance régulatoire et la surveillance prudentielle. En effet, la surveillance régulatoire se définit comme tout ce qui tient dans des équilibres efficaces des marchés qui ne peuvent les établir par eux-mêmes. Il s’agit donc d’un ensemble d’institutions et de règles qui portent sur les marchés et au regard desquelles les opérateurs sont des « boîtes noires ». La surveillance prudentielle, à l’opposé, s’assure de la solidité des opérateurs, c'est-à-dire s’introduit à l’intérieur des opérateurs et contrôle ainsi la solidité du capital, des fonds propres et quasi fonds propres, de l’organisation de la gouvernance de la société. La régulation est pour l’extérieur, le prudentiel est pour l’intérieur. Cette opposition s’est avérée catastrophique puisque précisément il y a communication entre l’intérieur et l’extérieur lorsqu’il s’agit des marchés financiers, puisque le marché financier est un marché d’information et que les informations sont conçues à l’intérieur des entreprises qui émettent les titres. Dès lors, il ne peut y avoir de régulation efficace que si il y a un prudentiel bien conçu, et l’opposition même n’a pas de sens ». Such dichotomy between regulatory and prudential, between macroeconomic risk and microeconomic supervision made no sense and blinded regulators from the implication their own sector, products or market participants had on other sectors. Two types of risks must be from now on looked out for: the one inherent to financial institutions themselves, such microeconomic risk which may have cause the second type of risk, the one posed to the system itself (the sector, for example banking, itself interconnected to financial market and therefore threatening the financial system as a whole)[32]: the first calls for prudential measures, the second for regulatory ones, both measures participating to building a governance mechanism of Regulation. The crisis shed the light on the vigorous need for information and transparency, as well as the need to verify one’s source, its exactitude, sincerity (a prudential requirement) and rightful circulation (between regulators and market participants). The Professor goes on: “de la même façon la crise a montré le continuum entre la fiabilité de l’organisation interne de certains opérateurs quant à leur organisation (ce fût un des enseignements de l’affaire Enron, qui avait 800 filiales) et la façon de gouverner l’entreprise et de communiquer l’information à l’intérieur de l’entreprise (corporate governance), avec la solidité du marché lui-même. C’est pourquoi les nouvelles réflexions de régulation financière mettent en lumière la notion d’ « opérateur systémique », qu’on pourrait aussi appeler « opérateurs cruciaux », et qui met à part des opérateurs dont le poids est si important sur le marché (critère de régulation) que leur organisation interne doit être spéciale ou particulièrement surveillée (critère prudentiel). Ainsi, régulation et gouvernance qui furent opposées, sont devenues indissociables ». The European financial supervision reform clearly reflects such thinking in both its architecture and objectives.

B) … abided by the new European supervisory architecture

Although negotiations on the new European architecture took over a year[33], many incidents during that period encouraged euro deputies to defend a more courageous reform than the one supported by member States (defending their national regulators) and proposed by the Commission. Clearly supporting the view that harmonization should prevail on protectionism, events such as “the Fortis bank crisis weekend, Germany's unilateral naked short-selling ban and the losses faced by life insurance policyholders in the UK, Ireland and Germany with the collapse of Equitable Life[34]” fully demonstrates that fragmentation is longer acceptable. On September 22nd 2010, euro deputies proudly fought for and obtained a stricter reform which allows for “the transformation of advisory committees into watchdogs with a bite”.

The Parliament, putting as priority number one information circulation and risk prevention, embraced the Larosière report, especially in regards to its architecture proposal, combining macro prudential and micro prudential supervision: on the one hand, A European System of Financial Supervision (ESFS) is to be established, regrouping all national and European actors of financial supervision, to act as a network. Three European supervisory authorities (ESA) will be created to replace the current “Level 3” supervisory committees (one for each particular financial sector: banking, insurance and securities), with more important powers (potentially expandable thanks to a review clause) than their current advisory nature. On the other hand, a European Systemic Risk Board (ESRB) will also be created in order to monitor and warn about the general circulation and accumulation of risk in the EU economic system.

The following figure describes what the Larosière report had in mind for the EU financial supervision architecture:

Regarding macroeconomic supervision, the ESRB, similar to what was recently implemented in the United States (Council of Systemic risk) by the Dodd Frank Act, it allows for a better and more timely warning about risk[35]. “The ESFS, chaired during the first five years by the Governor of the President Central Bank, will comprise the ESRB, the European securities and markets, banking and insurance supervisory authorities, the joint committee of the European supervisory authorities and Member States’ competent or supervisory authorities.

The ESRB has three main tasks: collect information, assess risk and warn the system when needed. First, it collects information and exchanges it. It has many tools to do so, such as the information that ESRB, the ESAs, the European system of central banks, the commission, the national supervisory authorities and national statistics authorities will be requested to provide, and other existing statistics produced and disseminated by the European Statistical System and the ESCB. More importantly, “if those data remain unavailable, the ESRB may request it from the Member State concerned, without prejudice to the prerogatives respectively conferred on the Council, the Commission (Eurostat), the ECB, the Eurosystem and the ESCB in the field of statistics and data collection”[36].

Second, should the Board identify a significant risk, it shall provide warnings (to the Commission, a member states, a national regulator or another European supervisory authority) and recommendations such as, when needed,legislative initiatives, on how to remedy to it. The Parliament also suggested mechanisms to enable the ESRB to communicate rapidly and clearly, such as a common color code to refer to different level of risk in order “to permit uniform ratings of the riskiness of specific cross-border financial institutions and make it easier to identify the types of risks they carry”[37]. The regulation proposed by the European Parliament also empowers the ESRB (as well as the Commission and ESAs) to ask the Council to declare an emergency.

Last but not least, the ESRB will have significant authority in regards to the follow-up of its recommendations. “Where a recommendation is addressed, the addressees shall communicate the actions undertaken in response to the recommendations to the ESRB and to the Council and provide adequate justification for any inaction ("act or explain"). Where relevant, the ESRB shall, subject to strict confidentiality rules, inform the ESAs without delay of the answered received” (art. 17(1) of the regulation).

The second important set of reform is the one regarding the creation ofa European System of Financial Supervision (ESFS), regrouping national regulators as well a new European supervisory authorities, bound to replace the current Level 3 advisory committees. “These Authorities would continue to perform all the current functions of the level 3 committees (advising the Commission on regulatory and other issues, defining overall supervisory policies, convergence of supervisory rules and practices, financial stability monitoring, oversight of colleges)”[38]. Its first mission is therefore to fight against fragmentation of supervisory and regulatory practices within the EU: “ The Authority shall establish, as an integral part of the Authority, a Committee on financial innovation, which gathers all relevant competent national supervisory authorities with a view to achieving a coordinated approach to the regulatory and supervisory treatment of new or innovative financial activities and providing advice for the Authority to present to the European Parliament, the Council and the Commission[39]”. The idea is that European supervisory authority, by editing common standards and methods of supervision addressed to national regulators and harmonizing the latter’s competencies and powers, ESAs will contribute to improving the quality of financial market supervision in the EU. And because, as the Larosière report underlines,rethinking the supervisory architecture is necessary but also goes hand in hand with improved rule making and regulatory rules, European supervisory authorities will also need to participate to EU law making. Regulatory mechanisms, supervision and crisis management are tightly linked and it would be inefficient to harmonize supervision practices throughout the EU while keeping fragmented national regulatory laws. For example, it would be unusefull to reform the EU supervisory architecture without clarifying technical standards needed to be implemented by national authorities or decide on a harmonize way in which a potential crisis would be handled and resolve by competent authorities. Therefore, ESAs will need to go on preserving and drafting coordinated and identical regulatory rules for all national regulators in regards to their supervision methods, standards, information gathering, implementing standards etc: “

contributing to the establishment of high- quality common regulatory and supervisory standards and practices, in particular by providing opinions to the Union institutions and by developing guidelines, recommendations, and draft regulatory technical and implementing technical standards which shall be based on the legislative acts referred to in Article 1(2) ; contributing to the consistent application of legally binding Union acts , in particular by contributing to a common supervisory culture, ensuring consistent, efficient and effective application of the acts referred to in Article 1(2), preventing regulatory arbitrage, mediating and settling disagreements between competent authorities, ensuring effective and consistent supervision of financial market participants, ensuring a coherent functioning of colleges of supervisors and taking actions,inter alia, in emergency situations[40]”.

In order for ESAs to fulfill their participate in regulatory standards and rules making, the Parliament and the Council delegate powers to the Commission so that is may directly adopt regulatory technical standards (technical standards shall be technical and not simply strategic decisions or policy choices) suggested by ESAs and in order to ensure consistent harmonization in these sectors. Once the ESA in question has drafted the technical standard in question, it will submit it to the Commission, which may not amend its content without prior coordination with the drafter (the Authority)[41]. Such provision offer ESAs with a true decisive role in the elaboration of Level 3 technical standards, since such mechanism allows for the authority’s interpretation (orientations, recommendations etc.) to become legally binding throughout the EU and for all national level financial institution or regulators.

Moreover,although the system does not deprive national supervisory authority of their power over national financial institutions (microeconomic regulation), the deal is somewhat changed with the new structure since national regulators will no longer be able to act as if they do not belong to and influence a supra national integrated market. Among their new powers, “the ESAs are set to get tough new powers to settle disputes among national financial supervisors and to impose temporary bans on risky financial products and activities. If national supervisors fail to act, then the authorities may also impose decisions directly on financial institutions, such as banks, so as to remedy breaches of EU law. The daily work of the ESAs will see them drive coordination within the current system of colleges of national supervisors set up to watch over cross-border financial institutions[42]” (such as for example credit rating agencies, soon to be directly supervised by the future European securities and market supervisory authority).

More specifically, in case of disagreement between national regulators, ESAs will be permitted to conduct a mediation between them, the outcome of which being legally binding on them. Further, when a dispute arises between two national regulators yet no agreement can be found on the situation of a financial institution under the jurisdiction of both regulators, the ESA will be allowed to impose supervisory decisions on the financial institution.

Further, the ESA will have an important role in the monitoring of national regulators, especially in regards to how they implement their obligation under EU law, such as their own supervisory assignments over national financial institution. If the concerned ESA deems that the national supervisory authority is in breach with its EU law obligations, it will be allowed to warn it and, if such instruction is ignored, the ESA will be allowed to directly instruct the financial institution to remedy to any breach of EU law. The regulation as submitted by the Parliament also provides that ESAs will be allowed to have significant authority on transnational financial institution. Such is the case for example for credit rating agencies, which will be under the direct supervision of the European Securities and Markets authority. As for the monitoring of national regulators themselves (and not merely their treatment of financial institution), the voted text provides, as J. de Larosière suggested, that “the Authorities would have a significant new responsibility of ensuring that all national supervisors meet necessary standards, by being able to challenge the performance by any national supervisor of its supervisory responsibilities, whether for domestic or cross-border firms, and to issue rulings aimed at ensuring that national supervisors correct the weaknesses that have been identified. In the event of the national supervisor failing to respond to this ruling, a series of graduated sanctions could be applied, including fines and the launch by the Commission of infringement procedures. In exceptional circumstances, where serious issues of financial stability are at stake, the Authorities should be able on a temporary basis to acquire the duties which the national supervisor is failing to discharge”[43].

Moreover, ESAs will have the important task to fulfill one of regulation’s most important objective: investor protection.In order to fulfill such goal, ESAs will “have the power to investigate specific types of financial institution[44], or financial products such as "toxic" products, or financial activities such as naked short selling[45], to assess what risks they pose to a financial market and issue warnings where necessary. Where specific financial legislation so provides, ESAs may temporarily prohibit or restrict harmful financial activities or products and may also ask the Commission to introduce legislative acts to prohibit such activities or products permanently[46]”.

This way, ESAs also participate to the most principal aim of market stability, since all of their micro economic supervision and activities will contribute to the ESRB’s mission, for example through the specific tasks conferred to them and the input such tasks offers them[47]. For example, the European banking supervision authority which will be in charge of systematically assessing financial practices and products of financial institution, and the European securities and market supervision authority will be in charge of supervising European credit rating agencies. ESAs will also have the power to ask the Council to declare an emergency situation. ESAs must also play along with the important objective to keep information available to investors and analysts, which also contribute to its own assessment of the financial system: “(fa) collect the necessary information concerning financial markets participants (…); (fb) develop common methodologies for assessing the effect of product characteristics and distribution processes on the financial position of financial markets participants and on consumer protection. (fc) provide a centrally accessible database of registered financial market participants in the area of its competence” (art. 6(2)) of the Parliament resolution).

Further, the ESAs also keeps a strong ex post imperium (in case a crisis occurs), necessary because « il est toutefois inévitable que des défaillances se produisent de temps à autre, et les modalités d’exercice de la surveillance doivent être examinées en ayant cela à l’esprit. Cependant, une fois qu’une crise a éclaté, les autorités de surveillance ont un rôle essentiel à jouer (conjointement avec les banques centrales et les ministères des finances) pour gérer la crise aussi efficacement que possible afin de limiter les dommages pour l’économie au sens large et la société dans son ensemble »[48].

Therefore, ESAs will be able to participate actively the creation and coordination of recovery and resolution plans as well as to procedures in emergency situations and preventive measures to minimize the systemic impact in the sector it monitors. And in crisis situation, Authorities keep an ex post authority on markets (e.g. they may temporarily prohibit certain practices or behavior in case of emergency situations) and have a coordinating role. Indeed, as an article of the Parliament’s regulation’s resolution underlines, ESAs will have a “permanent capacity to respond to systemic risks” and will have “capacity to respond effectively to the materialization of systemic risks (…) with respect to institutions that pose a systemic risk. The Authority shall (…) contribute to ensuring a coherent and coordinated crisis management and resolution regime in the EU[49]”.

Finally, what is perhaps the most remarkable provision imposed by the European Parliament, both ESAs and the ESRB’s powers, which can seem for the time being a little limited due to the remaining powers left to national regulators, may grow in the future in regards to future economic event and requirements (especially for example reviewing ESAs’ powers in regards to crisis management).“Particularly for the ESAs, MEPs ensured that the Commission will report back every three years on whether it is desirable to combine the separate supervision of banking, securities, and insurance on the benefits of having all the ESAs headquartered in one city and on whether the ESAs should be entrusted with further supervisory powers, notably over financial institutions with pan-European reach”.

C) Conclusion: beyond EU supervision: the need for a global one?

As a conclusion to this paper on regulation and supervision, it should be noted that, although the paper focuses on the recent European reform on supervision as an excuse to underscore the importance of supervision for regulated markets, the issue of supervision is also true and necessary at the global level. Indeed, while it is true that, notwithstanding market’s globalization and interconnectedness, no such global supervision or regulator exist at the moment, the advantages that such superior body could offer regulation (in particular regulation of global markets such as financial markets) can already be foreseen by the few meetings held within the G20. A concrete example is exactly the subject of this article: the European reform of financial supervision was triggered and completed according to what political leaders had decided on within the G20: “major failures in the financial sector and in financial regulation and supervision were fundamental causes of the crisis. Confidence will not be restored until we rebuild trust in our financial system. We will take action to build a stronger, more globally consistent, supervisory and regulatory framework for the future financial sector, which will support sustainable global growth and serve the needs of business and citizens”[50].

While the recent European reform could be seen as a proof that the G20 could fulfill such mission of international fora posing principles that nation states latter on will observe, it is no surprise that the EU indeed honored such commitments, since it was such regional organization which allowed for the first G20 meeting in 2008 in reaction to the crisis (see G2O’s meeting in Washington on November 15, 2008). Therefore, while the G20 “action plan” for financial markets (reinforce transparency, improvement if regulatory statutes and supervision, annihilate regulatory competition, intensify international cooperation etc.) seems to be having a true influence on its member states, yet international cooperation will not be truly efficient if no adequate representation of all international actors and national states, both from emerging region and developed ones, have a say in the matter, or else they will not have any incentive to implement principles into their national hegemonic legal system.

However, the EU (and also recently the United States) have proven that by transposing their G20 commitment into hard legal rules, a certain network of common principles is starting to arise at the international level. Moreover, the message that the EU or the US would have send the world would have they not transposed into their legal regimes their G20 commitment would have been, from the part of the world’s number one financial markets, catastrophic. Implementing such standards also avoids regulatory competition which is an important threat to the stability of global markets, and also encourages transnational commerce, both from financial institutions’ point of view (as they will be treated under the same regime in one place or in another), and from the regulator’s (supervisory standards being increasingly harmonized, facilitating benchmarking and therefore the supervision of the system as a whole).

Yet, such regulatory objectives cannot be reached without a coherent framework to draft and implement regulatory norms (at least a minima) and to cooperate on risk identification and coordination on global supervisory policies. For the moment, no global regulator in the sense of an institution with both ex ante and ex post powers over a regulated sector exists. Technical mechanisms to manage or prevent transnational risk or crisis is crucial to at least indicate lower scale authorities on how to regulate such market which are transnational. Without institution with an imperium over transnational financial institutions or national supervision authorities, the only timely possibility would be to rely on an international mechanism, possibly hosted by an already existing institution, which would gather national and regional opinions then set certain principles, standards and methods, and possibly gather supervisory information.

Jacques de Larosière suggests two paths to follow in order to encourage the convergence of such a coherent regulatory framework. “Firstly, a strengthening and broadening of bilateral

regulatory dialogues between the main financial centers. Secondly, a clear mandate, including precise objectives and timetables, for international standard-setters as currently discussed in the G20 context”[51]. The report clearly indicated that while a system based on mere “standard setting” could suffice in order to obtain harmonized supervision and regulatory practices and policies throughout the world, such quest will not be doable if no “hard” support is at the basis of such principles (the G20 having no legally binding rules or organization). Indeed, without legitimacy, such principles will not be taken into account by nation states. Such legitimacy could only be upheld if nation states themselves allow for a certain amount of their sovereignty relinquishment, left in the hand of an apparent impartial institution (recalling the importance that such institution be representative of all important economies). The Larosière report suggest to exploit the potential of the current Financial Stability Forum (FSF), although it does not, for the time being, reflects the minimal requirements necessary for such an organization to impose its views and regulatory standards on other lower level authorities. Based on what M. de Larosière suggests, the FSF could be transformed into a true regulator, in the sense that Marie-Anne Frison-Roche gives to the term: an institution with strong ex ante (e.g. rule making, risk detection) and ex post powers (e.g. standards and coordination of crisis management), still under a certain amount of requirements such as accountability (for example before the IMF), check and balance, neutrality, democratic (such as is the Basel Committee, which includes cooperation with market participants) yet technocratic (as a basis for its legitimacy) etc. (for example, as the European Parliament provided for new European supervisory authorities, “in order to fulfill its objectives, the Authority should have legal personality as well as administrative and financial autonomy”[52].

In this view, the FSF would reflect what Europe recently voted on, the European systemic risk Board, with mostly macroeconomic responsibilities and a macroeconomic supervision standard setting mission. But because half the risk developed on financial market come from inside market participants, calling for microprudential supervision, an architecture close to the second half of the European reform (the European System of financial supervision), also based on a network of supra national regulators, could permit to supervise transnational and systematically important financial institutions, as well as the task of surveying the enforcement by national regulators of regulatory and supervisory standards member states would have agreed on through the mean of such global body. There again, both macroregulatory and microprudential supervision would work together on market stability.

Finally yet ideally, in the long term, reflecting the system implemented for the World Trade Organization (WTO) –since such organization not only managed to implement hard legal rules on international trade, but also offers a dispute settlement body, permitting not only to settle dispute between States but also to create jurisprudence-, the Larosière report suggests to establish “a full international standard-setting authority, established by a treaty. The objective should be to put in place an international standard setting process which would be binding on jurisdictions and which would ensure implementation and enforcement of international standards[53]”.

But for the time being, it appears as such role is for the moment delegated to the IMF, which was recently appointed to monitor the financial state of 25 countries (including 15 of the G20). Indeed, on September 27 2010, the IMF announced the mandatory examination of 25 country’s financial system stability (such evaluation created in 1998 was up until now done on a voluntary basis). Experts mandated by the institution will study inter alia States’ crisis management mechanisms, carry on stress tests on financial institutions, analyse the facility for banks to have access to liquidity provided by central banks, as well as assessing one country’s bankruptcy law regarding financial institutions. The idea indeed is that, would have IMF experts been able to detect the dangerosity of the subprimes market and call on in time for a regorgnisaion of the american market, the crisis might have been avoid. “C’est donc une véritable mise à nu d’un système financier qui sera mise en œuvre afin d’éviter, autant que faire se peut, la répétition d’une crise comparable à celle qui sévit depuis plus de trois ans. Ce renforcement du rôle de surveillance du FMI s’inscrit en droit ligne des engagement des leaders du G20 de ne plus permettre un tel séisme et de mieux réguler l’activité du monde financier ». One can witness with this example that for global markets and transnational companies, in regions of the world which do not benefit from regional integration and organization such as the EU, other world regions also need a macroeconomic regulation (such as the “European Systemic Risk Council”), which is what the IMF, empowered by the G20, is currently intending to become. This proves that the architecture the EU will start benefiting from as from January 2011 is the right way to go and should be wishable for other regions of the world, since the amount of work suddenly put upon the IMF’s back will hardly sustain more regulatory and supervisory mission over its member states when the number of overviewed countries will start exceeding 25. Still, this also proves that multilateralism is not dead but rather is also a tool for efficient global Regulation.

[2] Enjeux les Echos, Interview of Jacques de Larosière « La cause du désastre, c’est le laxisme des autorités financières », Septembre 2010.

[4] The High Level Group on Financial Supervision in the EU, chaired by Jacques de Larosière, Brussels, February 25, 2009, §39.

[5] G. Galli et A. Mingardi, Lax Regulation Didn't Cause This Crisis : The Wall Street Journal, 29 janv. 2009, p. 15.

[6]European Commission, Financial Supervision, « Overview », available at : http://ec.europa.eu/internal_market/finances/committees/index_en.htm#overview

[7] Commission’s Press Release, “Financial services: Commission consults on review of Decisions establishing the Committees of Supervisors”, May 23rd 12008, IP/08/783. “At "Level 1", framework legislation setting out the core principles and defining implementing powers is adopted by co-decision after a full and inclusive consultation process in line with the better regulation disciplines. The technical details are formally adopted by the Commission as implementing measures at "Level 2", after a vote of the competent regulatory Committee (the European Securities Committee, the European Banking Committee and the European Insurance and Occupational Pensions Committee). In the Level 2 process the Commission takes careful account of the European Parliament's position. For the technical preparation of the implementing measures, the Commission is advised by Committees, made up of representatives of national supervisory bodies, referred to as the "Level 3" Committees – the Committee of European Banking Supervisors – CEBS, the Committee of European Insurance and Occupational Pensions Supervisors – CEIOPS and the Committee of European Securities Regulators – CESR. These Committees set up by Commission Decisions also have an important role to contribute to consistent and convergent implementation of EU directives by securing more effective cooperation between national supervisors and the convergence of supervisory practices. This is "Level 3" of the process. "Level 4" is where the Commission enforces the timely and correct transposition of EU legislation into national law. This four-level, comitology-based regulatory approach for financial services has been in place for more than five years in the securities sector and for more than two years in banking and insurance”. Communication from the Commission, “Review of the Lamfalussy process, Strengthening supervisory convergence”, 20.11.2007, COM(2007) 727 final, p.2

[8]See Article 32 (§2 and 4) of the Directive 2004/39/EC of the European Parliament and of the Council of 21 April 2004 on markets in financial instruments amending Council Directives 85/611/EEC and 93/6/EEC and Directive 2000/12/EC of the European Parliament and of the Council and repealing Council Directive 93/22/EEC, Official Journal L 145, 30/04/2004 P. 0001 – 0044. “Member States shall require any investment firm wishing to establish a branch within the territory of another Member State first to notify the competent authority of its home Member State and to provide it with the following information: (a) the Member States within the territory of which it plans to establish a branch; (b) a program of operations setting out inter alia the investment services and/or activities as well as the ancillary services to be offered and the organisational structure of the branch and indicating whether the branch intends to use tied agents; (c) the address in the host Member State from which documents may be obtained; (d) the names of those responsible for the management of the branch. (…) In addition to the information referred to in paragraph 2, the competent authority of the home Member State shall communicate details of the accredited compensation scheme of which the investment firm is a member in accordance with Directive 97/9/EC to the competent authority of the host Member State. In the event of a change in the particulars, the competent authority of the home Member State shall inform the competent authority of the host Member State accordingly.

[9] Larosière Report, p. 72

[10]Larosière report, p. 73

[11] The Lamfalussy process did not deal with strengthening prudential oversight – but the report warned: "While the committee strongly believes that large deep, liquid and innovative financial markets will result in substantial efficiency gains and will therefore bring individual benefits to European citizens; it also believes that greater efficiency does not necessarily go hand in hand with enhanced financial stability". Larosière’s report, p. 75