I-1.12 : The EU’s Financial Services Action Plan (FSAP) takes another step towards a liberal yet regulated single market in financial services through the Directive of July 2009 on UCITS.

The Directive innovates and improves the UCITS’ single market in three ways: first by recasting the 1985 Directive on UCITS in order to implement a simpler and harmonized regulatory framework (therefore improving UCITS’ marketing and investors’ protection) ; second, by providing for more cooperation between national and supranational regulators in order to secure and supervise UCITS’ single market ; third, by integrating the Directive into the Lamfalussy process as to ensure that its provisions be well-conceived, concurrently implemented by Member States and efficiently controlled by regulators.

FRENCH

La directive innove et améliore le marché interne des OPCV de trois façons : tout d’abord en réformant la Directive de 1985 sur les OPCVM de manière à instaurer un système de régulation plus simple et harmonisé (améliorant ainsi l’activité des OPCVM et la protection des investisseurs) ; en second lieu, elle met en place un meilleure coopération entre régulateurs nationaux et supranationaux de façon à sécuriser et mieux superviser le marché des OPCVM ; enfin, elle intègre la Directive dans le processus Lamfalussy afin de s’assurer de la qualité de ses dispositions, de sa transposition simultanée par les Etats Membres et de son contrôle effectif par les régulateurs européens.

GERMAN

Dank der OGAW Richtlinie von July 2009 richtet sich der Europäische Aktionsplan für Finanzdienstleistungen schritterweise nach mehr Liberalisierung sowie Regulierung der Binnenmarkt.

Die OGAW Richtline führt drei Reformen ein: Erstens wird die vorherige Richtlinie von 1985 verbessert, damit die Regulierung von OGAW leichter und harmonischer wird (und infolgedessen, damit der OGAW Betrieb und der Investorensschutz besser funktionnieren). Zweitens wird die Zusammenarbeit zwischen nationale- und europäische Regulierungsbehörde gefördert, um den OGAW-Markt sicherer zu machen. Und letztens wird die Richtlinie im Lamfalussy- Verfahren integriert. So werden die Qualität der Anordnungen der Richtlinie, ihre gleichzeitige Umsetzung der Richtlinie von Mitgliedstaaten und ihre tatsächtliche Überwachung auf der EU-Ebene gewährleistet.

SPANISH

Una Directiva visionaria sobre los OICVM: un nuevo paso hacia un mercado interno liberal, pero regulado en el sector de servicios financieros

La Directiva innova y mejora el mercado interno de los OICVM de tres formas: la primera, al relanzar la Directiva de OICVM de 1985 para poder implementar un marco regulatorio mas simple y harmonizado (lo cual mejora las acciones de los OICVM y la protección de los inversores); la segunda, al proveer más cooperación entre los reguladores nacionales y supranacionales para asegurar y supervisar el mercado de los OICVM; y la tercera, al integrar la Directiva en el proceso Lamfalussy para asegurar la calidad de sus disposiciones, su transposición simultanea para los Estados Miembros y su control eficaz por los reguladores europeos.

The Directive innovates and improves the UCITS’ single market in three ways: first by recasting the 1985 Directive on UCITS in order to implement a simpler and harmonized regulatory framework (therefore improving UCITS’ marketing and investors’ protection) ; second, by providing for more cooperation between national and supranational regulators in order to secure and supervise UCITS’ single market ; third, by integrating the Directive into the Lamfalussy process as to ensure that its provisions be well-conceived, concurrently implemented by Member States and efficiently controlled by regulators.

Directive 85/611/EEC of 20 December 1985 on the coordination of laws, regulations and administrative provisions relating to undertakings for collective investment in transferable securities (UCITS) has largely contributed to the development and success of the European investment funds industry. However, when it became clear that changes needed to be introduced into the UCITS legal framework in order to adapt it to the financial markets of the twenty-first century, the Commission’s Green Paper of 12 July 2005 on the enhancement of the EU framework for investment funds launched a public debate on the way in which Directive 85/611/EEC should be amended in order to meet those new challenges. That intense consultation process led to the largely shared conclusion that substantial amendments to that Directive were needed, which led to the conclusion that it should, in the interests of clarity, be recast rather than simply amended. “As part of the Commission's Better Regulation Strategy and its firm commitment to simplify the regulatory environment, the new Directive will replace 10 existing directives with a single text” (it is therefore sometime referred to as UCITS IV)[1].

In a nutshell, the changes to the UCITS Directive remove administrative barriers to the cross-border distribution of UCITS funds, create a framework for mergers between UCITS funds, allow the use of master-feeder structures, replace the Simplified Prospectus by a new concept of Key Investor Information and improve cooperation mechanisms between national supervisors.

1)Directive’s main objectives, at the heart of the EU’s Financial Services Action Plan

The directive’s main objective is to implement a true internal market for UCITS by coordinating existing national laws governing them (as it facilitates the removal of the restrictions on the free movement of units in the community), in the interest of investors (unitholders) and of managements companies. This broad goal is bound to be achieved thanks to the following measures:

-the directive provides for common basic rules for the authorization, supervision, structure and activities of UCITS established in Member States and the information that they are required to publish.

-Moreover, the directive provides that any authorization granted to the “management company in its home Member State should ensure investor protection and the solvency of management companies, with a view to contributing to the stability of the financial system”. Indeed, harmonization will secure the mutual recognition of authorization and of prudential supervision systems, in order to make possible the grant of a single authorization valid throughout the Community and the application of the principle of home Member State supervision (§8).

-Therefore, “By virtue of the principle of home Member State supervision, management companies authorized in their home Member States should be permitted to provide the services for which they have received authorization throughout the Community by establishing branches or under the freedom to provide services” (§11).

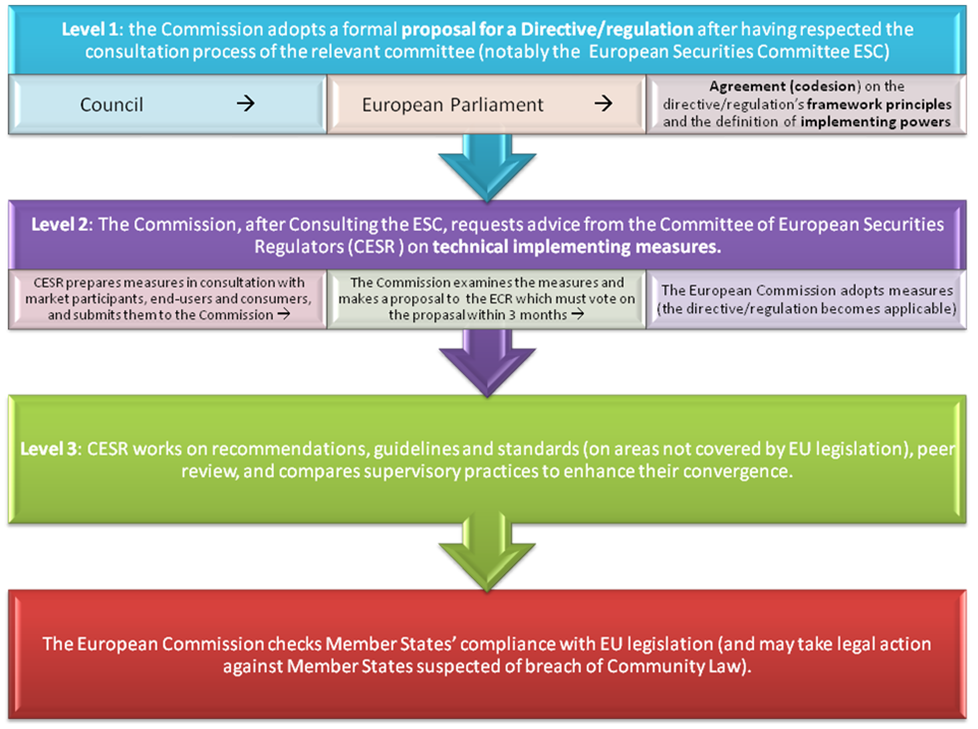

The UCITS IV Directive not only updates and recasts the last directive on UCITS (which dates back to 1985) but also integrates it into the Lamfalussy process: the directive becomes a level 1 measure, which awaits for level 2 implementing measures to put it into practice (measures without which the Directive still awaits its final adoption[2]). Regarding those level 2 measures, the Commission sent on 13 February 2009 to the Committee of European Securities Regulators (CESR) a 'provisional request for technical advice on the new UCITS Directive implementing measures'. The provisional request has been divided into three parts: “Part I covers priority areas where the Directive obliges the Commission to adopt implementing measures. They mostly aim at securing the smooth operation of the management company passport. Part II is devoted to implementing measures which allow the key investor information to become an operational tool. Part III covers areas such as fund mergers, master/feeder structures and the notification procedure” [3]. CESR delivered on April 2010 its advice on these matters, which are indeed the highpoints of the new Directive. The Commission will need to take notice of these feedbacks in order to legislate, before July 1st 2010, on these Level 2 measures (implementing measure taking the form of either a regulation or a directive), bound to complete the UCITS IV and to render it applicable by Member States.

2)Directive's improvements on measures related to Merger of UCITS

In order to improve the functioning of the internal market, the Directive lays down Community provisions facilitating mergers between UCITS, so that cross-boarders mergers between all types of UCITS (contractual, corporate and unit trusts) be “permitted and recognized by each Member State without the need for Member States to provide for new legal forms of UCITS in their national law” (§27)[4]. The Directive tries at the same time to facilitate those cross-boarders mergers while protecting the investor.

First, cross-boarders mergers will only be submitted for approval to the competent authorities of the merging UCITS home Member State (rather than those of the receiving UCITS, art. 39). Moreover, the authorization will not be granted if the merging and receiving UCITS failed to provide appropriate and accurate information on the proposed merger to their respective unitholders, or should the merger appear as imposing extra-costs upon the latter[5], which participates to the protection of investors. Indeed, the merging and receiving UCITS must provide appropriate and accurate information on the proposed merger to their respective unitholders “so as to enable them to make an informed judgment of the impact of the proposal on their investment” (art. 43-1). Finally, unitholders may require additional information, “and the right to request the repurchase or redemption or, where applicable, the conversion of their units without charge” (art. 43-c). The authorization shall not be granted if the merging and receiving UCITS failed to provide appropriate and accurate information on the proposed merger to their respective unitholders, or should the merger appear as imposing extra-costs upon them[6]. The competent authorities of the merging UCITS home Member State will inform the merging UCITS whether or not the merger has been authorized (art. 39-5) within 20 working days of submission of the complete information.

CESR, in its feedback to the Commission in order to put together Level 2 implementing measures on mergers, mainly focused on the information to be provided to unitholders. It solely suggested “some clarification on the distinction to be made between information provided to unitholders in the merging UCITS and the receiving UCITS, as well as on the content of the information to be included with a view to allowing unitholders to make an informed decision”[7].

3)Recognition of master- feeder structures

Already at play in some European countries such as France, the Directive acknowledges the system called master-feeder structure. According to the Directive, a feeder UCITS is a UCITS which has been approved to invest at least 85 % of its assets in units of another UCITS or investment compartment thereof (the master UCITS). By recognizing this system at the EU level, the Directive therefore allows for example a feeder based in Luxembourg to have a French Master.

A feeder UCITS may hold up to 15 % of its assets in ancillary liquid assets or financial derivative instruments (which may be used only for hedging purposes) or in movable and immovable property which is essential for the direct pursuit of the business if the feeder UCITS is an investment company (art. 58).

The investments made in a master UCITS by a feeder must be subject to prior approval by the competent authorities of the feeder UCITS home Member State (art 59). Moreover, the Directive provides for a list of compulsory information and marketing communications to be issued by the feeder UCITS (art.63).

As for CESR’s advice in this area (in order to assist the Commission in the drafting of implementing measures –Level 2 measures in the Lamfalussy approach), it focuses on the content of the written agreements that should be put in place between the master and feeder UCITS as well as their respective depositaries and auditors, “while reaffirming its view that there should at all times be equitable treatment of all unitholders”[8].

4)Improvements regarding the notification procedure for cross-boarders marketing

The objective that UCITS should be able to market their units in other Member States subject to a notification procedure is not a novelty. However, the 2009 Directive does improve the system in many ways. First, the Directive shortens the notification time frame to the host country’s regulator from 2 months to 10 days. Moreover, the Directive improves the communication between the competent authorities of Member States, as it allows that the notification file be sent to the host country’s regulator by the competent authorities of the UCITS home Member State rather than the company itself[9].This way, “it should not be possible for the UCITS host Member State to oppose access to its market by a UCITS established in another Member State or challenge the authorization given by that other Member State” (§62). Furthermore, to facilitate the access to the markets of other Member States while protecting investors, the Directive provides for the simplification of the number of languages used for the notification process: “the UCITS should be required to translate only the key investor information into the official language or one of the official languages of a UCITS host Member State or a language approved by its competent authorities” (§66).

Finally, the Directive delegates to the Commission the task to take implementing measures specifying “the form and contents of a standard model notification letter to be used by a UCITS for the purpose of notification; (…) the form and contents of a standard model attestation to be used by competent authorities of Member States (…), [and] the procedure for the exchange of information and the use of electronic communication between competent authorities for the purpose of notification”. In assistance to the Commission, CESR completed on April 19th 2010 its guidelines regarding these matters, especially on the electronic transmission of notification files (i.e. through the development of a dedicated electronic system to effect transmission of notifications between competent authorities). It appears that this suggestion was well received by Member States and that CESR “will carry out further work to assess the pros and cons of the different types of IT system that could be developed with a view to introducing greater automation to the notification process” (CESR also confirms its own proposal to use emails in case no dedicated system is made available)[10].

5)Improvements regarding Key investor information (KII)

The Directive replaces the Simplified Prospectus by a new concept of Key Investor Information (KII), i.e.marketing communications and obligatory investor disclosures by UCITS. Obligatory investor disclosure includes key investor information, the prospectus and annual and half-yearly reports (§59). Key investor information should be provided as a specific document to investors, free of charge, in good time before the subscription of the UCITS, in order to make sure investors reach informed investment decisions. Because the previous Directive provided for too complicated key information (prospectus), such key investor information should from now on only contain the essential elements for making such decisions. Moreover, the key investor information’s content is harmonized in order to ensure that investors are protected and have sufficient information to enter comparability assessments. The key investor information’s format is also modified by the Directive and must, from now on, be short (i.e. “a single document of limited length presenting the information in a specified sequence is the most appropriate manner in which to achieve the clarity and simplicity of presentation that is required by retail investors, and should allow for useful comparisons, notably of costs and risk profile, relevant to the investment decision”, §59). Key investor information provides information on the UCITS’s identification, a short description of its investment objectives and investment policy, a presentation of its past-performance presentation (and if possible performance scenarios), costs and associated charges and risk/reward profile of the investment, “including appropriate guidance and warnings in relation to the risks associated with investments in the relevant UCITS” (art.78).

The Directive finally provides that a level 2 regulation (implementation measures) will have to be taken on the format and content of Key Information Document disclosures for UCITS, and the methodology for the calculation of the synthetic risk and reward indicator. The Commission, in charge of implementing these level 2 measures, called on CESR for technical advice. The latter confirmed its preference for a synthetic risk and reward indicator accompanied by a narrative text. CESR recommends however that (i) information on the possible impact of a fund’s Home State taxation regime should be disclosed in the KID, and (ii) that when past performance are not adapted to certain types of funds (e.g. structured funds such as formula funds, capital protected funds and comparable funds), “the objectives and investment policy disclosure should be supplemented by performance scenarios which illustrate the risk and reward trade-offs of the fund”[11]

6)Implementation of a management company passport

The directive also improves cooperation mechanisms between national supervisors, especially as regards the "management company passport" (i.e. the possibility for funds authorized in one Member State to be managed remotely by a management company established in another Member State), regarding which the pre-Directive consultation process revealed potential supervisory and investor protection concerns. The idea of a company passport is coupled with the present Directive’s principle of home Member State supervision: “management companies authorized in their home Member States should be permitted to provide the services for which they have received authorization throughout the Community by establishing branches or under the freedom to provide services” (§11). Management companies can therefore create and manage UCITS based in other Member States, without establishing or keeping any structures in their home Member State. The passport idea was already provided for in the Directive 2004/39 (the Markets in Financial Instruments Directive, MiFID) and is the direct consequence of the transposition into national law of the free establishment principle (art. 532-16 of the French Monetary and Financial Code).

Close to the notification procedure for cross-boarders marketing (the notification being done by the home state’s regulator to the host state’s one), it is for the competent authorities of the management company’s home Member State (within two months of receiving all the information included in the notification for the establishment of a branch within the territory of another Member State) to communicate that information to the competent authorities of the management company’s host Member State (art.17). Therefore, any French Management company may manage a Luxembourg UCITS (the only condition being that the depositary, i.e. the entity entrusted with the assets of a common fund for safe-keeping, be of the same nationality as the managed UCITS).

Moreover, when a UCITS is managed by a management company authorized in a Member State other than the UCITS home Member State, that same management company must adopt procedures to deal with investor complaints and also establish procedures to make information available at the request of the public or the competent authorities of the UCITS home Member State (through a contact person chosen among the employees of the management company to deal with requests for information - §19). However, such a management company does not need (and cannot be obliged by the law of the host Member State) to have a local representative in that Member State in order to fulfill those duties of information and complaints gathering (§19).

Finally, the duty and responsibility for supervising “the adequacy of the arrangements and organization of the management company so that the management company is in a position to comply with the obligations and rules which relate to the constitution and functioning of all the UCITS it manages” (art.19-7) is put upon the authorities of the management company’s home Member State.

In the same way it was done for the cross-boarders marketing notification, the mergers and the master-feeder’s provisions, the Directive also provides that the rules on management company passport will have to be coupled with a set of Level 2 measures (implementing measures) that the Commission, with CESR’s Level 3 assistance, must adopt before July 1st 2010 in order for the Directive to be fully applicable within July 1st 2011. CESR delivered its advice on this matter on 28 October 2009. It focuses on “the requirements on organizational arrangements, conflicts of interest and rules of conduct for management companies; risk management; additional measures to be taken by depositaries; and issues related to supervisory co-operation”[12].

7)Conclusion

This new Directive is at the heart of the EU's Financial Services Action Plan (FSAP). Indeed, it participates to the FSAP’s main objective: the improvement of the single market in financial services. Its new provisions should increase the legal framework's efficiency of investors’ protection. First, UCITS' managers will be able from now on to develop cross-boarders activities without extra costs, therefore allowing for economies of scale and saving consolidation. Indeed, based on the Commission’s data, European UCITS are 5 times more important than American ones although their management costs are twice as high. As for investors, they will benefit from a wider choice of UCITS and more transparent, easy-to-understand information. “These improvements will help reinforcing the competitiveness of UCITS on global markets. Currently 40 % of UCITS originating in the EU are sold in third countries, mainly Asia, the Gulf region and Latin America (…). This legislative package should ensure that the UCITS rulebook continues to be a success story in Europe and also in other parts of the world, like Asia or Latin America, where the UCITS brand is widely sold and highly valued"[13]. From that point of view, it appears as if the Directive will enhance regulatory environment and provide for cost savings (i.e. reduce unnecessary costs and bureaucracy in cross-boarders operations) and investor’s transparency. As Internal Market and Services Commissioner Charlie McCreevy underscores, “the expected benefits of this package to the EU industry are estimated to more than €6 billion. We expect these benefits to lead to lower costs for investors. During the last years, we have carefully identified the areas where improvement in existing provisions needed to be introduced. This was done on the basis of an extended consultation process and in-depth cost-benefit analysis”[14]. However, one will need to wait for the Directive’s implementation by Member States (July 11th 2011) to witness the expected efficiencies.

Moreover, one must also wait July 2010 to find out which of CESR’s recommendations the Commission decided to include in its implementing measures (themselves submitted to the approval of the European Securities Commission – ESC) in order for the Directive to be fully applicable by Member States before July 1st 2011.

However, one may already recognize the efficiency of the Lamfalussy process, thanks to which the main values of European legislation are implemented by the Council and the Parliament at the 1st Level, while technical details are delegated to the Commission (Level2), itself assisted by one of the Level 3 committees (either the Committee of European Insurance and Occupational Pensions Supervisors - CEIOPS, the Committee of European Banking Supervisors –CEBS or, which is the case for UCITS IV, the Committee of European Securities Regulators –CESR).

This process indeed makes sense as it increases the efficiency of European Legislation. General policies should indeed be taken by institutions in charge of defining the general political direction and priorities of the European Union (such as the Council), where technical matters should be left in the hands of technocratic institutions, such as regulators, close to the sector and more apt to not only suggesting propositions adapted to the requirements of such and such sectors, but also at submitting them to each national regulator before making the synthesis of each Member States’ advice. Therefore, when helping the Commission to take decisions on Level 2 implementing measures, the relevant Level 3 Committee (in case of securities regulation, CESR) is closer to market participations, end-users and consumers. It is in a better place to judge which technical measures should be taken in order for the Directive to be fully applicable by Member States and to fulfill its objectives (lower costs, better investor information etc.). Moreover, such Level 3 institution does not only help the Commission in deciding on Level 2 implementing measures but also has specific tasks regarding the Lamfalussy process’s Level 3. Level 3 is bound to call on the relevant committee (in case of financial markets issues, CESR) which must work on recommendations, guidelines and standards (areas not covered by EU Legislation), peer review and compare supervisory practices to enhance their convergence. These Level 3 tasks being these Level 3 institutions’ daily job, they become increasingly experts in the sector they are regulating. Therefore, it makes perfect sense that, according to the Lamfalussy process, these institutions are called-on by the Commission to advise it on Level 2 implementing measures, that is to say very technical and detailed suggestions on how to put into practice the Directive/Regulation’s main values and principles as it was conceived by the Council and the Parliament.

For example, in the case of the UCITS IV Directive’s objective to improve cooperation mechanisms between national supervisors as regards the "management company passport", the Commission decided to consult the Committee of European Securities Regulators (CESR). CESR was therefore invited to provide advice as to help the Commission to develop provisions permitting the introduction of a management company passport under conditions that are consistent with high level of investor protection. After making an assessment on how investor protection may be deteriorated and how to make sure that UCITS brand remains a gold standard, CESR advices the Commission on the structure and principles which could guide potential future amendments to the UCITS directive which may be needed to give effect to the UCITS management company passport. After such process, and after having consulted market participants, end-users and consumers (i.e. after getting information from the sector itself), and having submitted its suggestions to national regulators which may express their opinion based on their own national experience, CESR’s feedback will permit the Commission to come forward with an appropriate and informed proposal in time to allow for the Directive’s adoption.

In this regards, the Directive’s main improvement does not only rely in its objectives and material provisions (enhance the internal market, protect investors etc.) but in the fact that its elaboration was integrated in the Lamfalussy process which provides several benefits over traditional lawmaking, including more-consistent interpretation, coordination between national supervisory practices, and an overall improvement in the quality of legislation on financial services. The Lamfalussy process, which became famous for its efficient application in the drafting of the Directive on Market in Financial Instruments (MiFID), and was even more recently used to implement the Solvency II regulation, once again demonstrates how it participates to fulfill the EU Financial Services Action Plan (FSAP). Indeed, the Lamfalussy approach was used to implement "level 1 Directives" such as the MiFID, the Market Abuse Directive, the Prospectus Directive and the Transparency Directive which are crucial pieces of legislation and which form an essential part of the Commission’s Financial Services Action Plan. Moreover, not only does the approach implements an innovating legislation process ("level 1 Directives" set out framework principles and "level 2 Directives" set out the implementing measures that allow these principles to be put into practice) it also puts “the spotlight on those Member States that are lagging behind. This will put them under pressure to improve their performance as quickly as possible”[16] and implement Level 1 and 2 measures in a harmonized, supervised and efficient manner.

[2]N.B.: the Lamfalussy process was established in order to improve the making of regulations within the EU (in particular for financial services regulation). Developed by Alexandre Lamfalussyin 2001, it is made up of four "levels," each playing a specific part in the drafting, enforcing, implementing and controlling of such EU legislation. The “first level” refers to the adoption by the EU Parliament and the Council of the EU of a certain piece of legislation, the latter only providing for the main objectives of the law and the ways in which it shall be implemented. The legal text then passes to the second level: it is sent to a sector specific committee which gives a consultation on technical aspects of the text, with the help of national regulators (before bringing it to a vote of member-state representatives). This feedback statement on technical details is bound to assist the Commission in adopting the implementing measures in order for the text to be fully applicable in Member States. The third level is the coordination between national regulators on the implementation measures they took to apply the EU law within national law, in order for the new regulation to be similar in all member states. Finally the fourth level is bound to ensure the compliance of national regulations to the EU text.

[4] The cross-border merger of UCITS aimed at by the Directive are those are those involving “ (i) at least two of which are established in different Member States; or (ii) established in the same Member State into a newly constituted UCITS established in another Member State” (art. 2, q). A ‘domestic merger’ means a merger between UCITS established in the same Member State where at least one of the involved UCITS has been notified pursuant to Article 93 (on the notification for cross-boarders marketing).

[11] CESR, 19 April 2010, Ref.: CESR/09-995, Feedback statement ; CESR’s technical advice to the European Commission on the format and content of Key Information Document disclosures for CESR’s technical advice to the European Commission on the format and content of Key Information Document disclosures for UCITS.

{kind=link}

your comment